Value Added Tax shall be governed by the provisions of the attached law.

ATLA

Law No. 67-2016 Value Added Tax Law

No matches found.

ATLA's AI Assistant

Preamble

Preamble

In the Name of the People,

The President of the Republic,

The House of Representatives passed the following law and it is hereby issued,

Clause (I)

Clause (II)

General Sales Tax Law No. (11) of the year 1991 shall hereby be repealed. All provisions contrary to the provisions of the present law shall hereby be repealed. Conciliation and grievance committees formed in accordance with the provisions of abovementioned Sales Tax Law shall continue to review tax appeals referred thereto for three months, provided that thereafter, the unresolved appeals shall be referred to the Committees stipulated in the attached law.

Clause (III)

"Sales Tax Department (STD)" phrase, whenever mentioned in laws, decrees and regulations in force shall be replaced by the "Egyptian Tax Authority (ETA)".

Clause (IV)

Registrants, under the provisions of General Sales Tax Law, shall keep their registration number in case their sales reach and/or exceed the threshold stipulated in the attached law. Importer of taxable goods as well as each and every manufacturer and/or importer of a commodity from the table attached to the General Sales Tax Law if the same commodity is included in the table accompanying this law, shall remain registered hereunder regardless of volume of transactions thereof and shall observe the provisions of attached law.

Such persons shall pay due sales tax and file relevant returns on the due dates stipulated herein and shall keep relevant books, records and documents for the five years following enactment of such law according to terms and conditions stipulated in the Executive Regulations thereof.

In case of violation of any of the provisions stipulated in the two preceding paragraphs, the registrant shall be deemed a tax evader under the provisions of the attached law.

ETA may, based on any available in-hand data or documents, amend tax returns and may take due legal actions to collect due sales tax. The registrant may appeal such actions under the provisions of the attached law.

Clause (V)

A registrant whose turnover is below the threshold stipulated in the attached law shall be automatically deregistered, unless such registrant is required to continue to be registered within sixty (60) days as of the enforcement date of this law. All deregistered persons shall file a tax return for such tax period preceding deregistration as well as tax periods whose relevant returns have not been deemed due yet within thirty (30) days as of the enactment date of the present law stating the closing balance of finished products, raw materials and services. All deregistered persons shall pay the General Sales Tax due within six (6) months as of enforcement date of the present law and shall keep books, records and documents for the five (5) following years of deregistration as well as provide access of such to ETA staff.

ETA may, based on any available in-hand data or documents, amend tax returns and may take due legal actions to collect due sales tax. The registrant may appeal such actions under the provisions of the attached law.

Clause (VI)

Registrants may, in accordance with provisions of the present law, deduct any credit balance of the deductible General Sales Tax prior to the enforcement of the current law, as well as any amounts that have not been fully deducted or refunded of the Sales Tax amounts paid on machines, equipment as well as parts and spare parts thereof in addition to tax previously paid on sales’ returns. Such registrants may deduct Table Tax due on vehicles in their possession from sales tax previously paid on same vehicles as per terms and conditions stipulated by the Executive Regulations.

The General Sales Tax previously paid on exported goods, services or inputs thereof as well as tax paid by mistake shall be refunded in accordance with procedures and rules stipulated in the attached law.

Clause (VII)

Without prejudice to the provisions of the present law and the attached law, persons who continue to be registered under the provision of the present law or persons who will be registered in accordance with the attached law shall adapt their position to the VAT law within three months as of law enforcement date. During this period, registrants shall be exempted from the additional tax of the due tax and Table Tax differences in case calculation of tax depends on conciliation thereof. The Executive Regulations stipulates Decrees and rules relevant to conciliation.

Clause (VIII)

The provisions of the present law and the attached law shall not affect exemptions stipulated by virtue of agreements concluded between the Egyptian government and foreign countries, international or regional organizations, or petroleum and mining agreements.

Clause (IX)

The Minister of Finance shall, within thirty (30) days of the promulgation of the present law and the attached law, issue the Executive Regulations thereof. Until the Executive Regulations is issued, currently in force regulations and decisions shall be effective provided that such are not contrary to the provisions of these two laws.

Clause (X)

The attached law shall be published in the official Gazette and shall come into force as of the following day of publication and shall receive the Seal of State and be implemented as a State law.

Issued by The Presidency of the Republic on:

Date: Dull-Hijja 03, 1437 AH

Corresponding to: September 05, 2016 AD

Abd Elfattah Elsisi

Section I Definitions

ARTICLE (1)

In the application of the provisions herein, the following terms and phrases shall have the corresponding meanings hereunder:

Minister : Minister of Finance (MOF)

Commissioner of ETA : Commissioner of the Egyptian Tax Authority

Authority : Egyptian Tax Authority (ETA)

Taxable Person : Natural or juridical person, public or private, who is required to collect and pay the tax to ETA whether said person is a taxable commodity or service producer, trader or service provider whose sales reaches the threshold stipulated herein as well as importers, producers or distribution agents of taxable commodity or service regardless of their turnover, as well as producers and importers of commodities and services stipulated in the table attached to the present law regardless of their turnover.

Registrant : Taxable person who is registered at ETA in accordance with the provisions of the present law.

Associated Person : Any person who is related to another in a way that affects the determination of the tax base including:

1. Spouse, antecedents and descendants;

2. A corporation and the person who directly or indirectly holds at least (50%) of the number or value of shares and/ or voting rights thereof;

3. Partnerships, active partners and silent partners(1);

4. Any two or more enterprises in each of which another person holds at least (50%) of the number or value of shares and/ or voting rights in each.

5. Employer and affiliated staff who are related to the employer with business relationships.

Service Provider : Each natural or judicial person who supplies or provides a taxable service.

Importer : Each natural or judicial person who imports taxable sales or services regardless of the purpose of import.

Resident : Each natural or judicial person who is settled in Egypt under the provision of the income tax.

Permanent Establishment :

The premises in which the business operations are carried out, including:

1. Administrative headquarters.

2. Branches, office, factory or workshop.

3. Mine, oil field, gas well, quarries or any other place extracting natural resources.

4. Building sites or construction or installation projects.

Such persons who have a permanent establishment in Egypt shall be obligated by the present law.

Tax : Value Added Tax

Additional Tax : Additional tax of 1.5% of unpaid VAT or Table Tax including due tax resulting from amendments of the tax returns for each or part of the month as of the end of the period specified for payment until the payment date.

Input tax : Tax paid by the taxable person upon purchasing or importing goods including machines, equipment and services, whether direct or indirect, related to selling taxable goods or provision of taxable services.

Table Tax : A tax imposed at definite rates or values on the sale or importation of local or imported goods and services stipulated in the table attached herein, other than the tax stipulated in the first paragraph of Article (2) herein unless otherwise enumerated in the attached table.

Commodity : Every material thing, regardless of nature, source or purpose thereof including electric energy, whether local or imported. The definition of a commodity shall be guided by comments and provisions of the items stipulated in sections and chapters stipulated in the in force Customs Tariff Table.

Service : Anything other than any commodity whether local or imported.

Exempted Goods and Services : Goods and services included in the exemption lists attached hereto

Sale : Transfer of the commodity ownership or service provision from the seller, even importers, to the purchaser. According to the provisions hereto, any of the following shall be deemed sale, whichever precedes:

1. Issuance of an invoice;

2. Delivery of goods or provision of services; and

3. Wholly or partially making payments, down payments, credit sale or any other form of payment for goods and/ or services as per different payment terms and conditions.

Tax Invoice : Invoice prepared according to form issued by a decree of the Minister or his authorized representative.

Month : Calendar month

Tax Period : A period of a month that elapses at the end of each Gregorian month for which registrants submit monthly tax returns.

Fiscal year : A twelve-month period starting and ending with the fiscal year of the taxable person.

Personal Consumption : Use of a commodity or benefiting from a service for purposes other than business operations.

Special Usage : Use of a commodity or benefiting from a service for purposes related to business operations. Transfer of a commodity from one production stage to another inside or outside the facility shall not be deemed a special usage.

Non-resident registrant(2) : Natural or legal person who is non- resident in Egypt and shall be deemed liable to register in and charge VAT upon sale of goods and provision of imported services to non-registrant clients in Egypt.

Simplified supplier registration system(3) : A system allowing registration of non-resident suppliers in such simplified way as defined by The Executive Regulations

Reverse Charge system(4) : A system according to which beneficiary of goods or services shall directly pay tax to ETA instead of non-resident supplier of goods or provider of service in such cases set herein.

(1) The sentence of "active partners and silent partners" was added by the retraction published in the Egyptian Gazette, Edition No. (44), issued on 03/11/2016. Attached at the last page herein.

(2) Added by Law No. (3) of 2022 - Egyptian Gazette Edition bis (3 E), issued on January 01, 2022.

(3) Added by Law No. (3) of 2022 - Egyptian Gazette Edition bis (3 E), issued on January 01, 2022 .

(4) Added by Law No. (3) of 2022 - Egyptian Gazette Edition bis (3 E), issued on January 01, 2022 .

Section II Value Added Tax

Chapter I Tax Application and Chargeability

ARTICLE (2)

Tax shall be charged on goods and services including goods and services listed in the table attached hereto, whether local or imported, in all stages of transactions, unless otherwise specified by a special provision.

An amount of 40 piasters of tax collection imposed on serial (First:1/B/3) of Table (1) attached herein shall be allocated to General Authority for Health Insurance and minister of Finance shall define in agreement with Minister of Health such rules governing payment of such amount to General Authority of Health Insurance by virtue of a decree issued by Minister of Finance.(5)(*)

(5) Paragraph (2) of Article (2) was added by Law No. (3) of 2017 - Official Gazette - Edition (2 bis B) issued on January 15, 2017.

(*) Law No. (2) of 2018 was promulgated to issue "Universal Health Insurance System" and Article 40 thereof, item 9 reads as follows:-

Ninth: Other sources:

The following amounts shall be collected according to this law to finance such system:

- 75 piasters of value of pack of cigarettes in local market whether local or foreign production providing increase of such value by 25 piasters every three years to reach 150 piasters.

- (10%) of value of every sold unit of tobacco derivatives other than cigarettes.

- one pound to be collected upon passage of every vehicle on such high ways that are subject to such fare collection system.

- 20 pounds for every year upon issuance or renewal of driving licenses.

- 50 pounds for every year upon issuance or renewal of car licenses of litre capacity of less than 1.6 litre.

- 150 piasters for every year upon issuance or renewal of car licenses of litre capacity of 1.6 litre or less than 2 litre.

- 300 pounds for every year upon issuance or renewal of car by licenses of litre capacity of 2litres or more.

- An amount ranging from 1000 to 1500 pounds upon contracting with such system for medical clinics and centers, pharmacies and pharmaceutical companies according to rules set by The Executive Regulations of this law.

- 1000 pounds per bed upon issuance of licenses of hospitals and medical centers.

- Solidarity contribution at 0.0025% (2.5 x1000) of total annual revenues of sole-proprietorship and companies regardless of nature or legal status thereof, as well as public economic entities. Such contributions shall not be deemed part of deductible costs in application of provisions of Income Tax Law and shall be collected according to controls and procedures set forth by The Executive Regulations thereof.

ARTICLE (3)

Standard VAT rate on goods and services shall be (13%) for fiscal year 2016/2017, and shall be (14%) as of the beginning of fiscal year 2017/2018, provided that a percentage of (1%) of tax shall be allocated to expenditure on social justice programs. As an exception from the above, tax rate on machines and equipment used in manufacturing a commodity or provision of a service shall be 5% except for buses and passenger cars.

Such goods and services exported under the terms and conditions stipulated by the Executive Regulations shall be zero-rated.

ARTICLE (4)

Taxable persons shall collect and pay VAT to ETA according to deadlines specified herein.

ARTICLE (5)

Upon selling a commodity and/or providing a service by taxable persons in all stages of transactions, tax shall be charged as per the provisions stipulated herein regardless of the method of selling of goods or rendering of services as well as dealing in such including online means.

Imported goods shall be taxed, regardless of the purpose of import including personal consumption or special use, in the customs release stage upon the ascertainment of customs duty point. Tax shall also be charged upon Customs release throughout all transaction stages of the goods in Egypt. Rules related to special customs regimes shall be applied on imported goods unless otherwise stipulated by virtue of a special provision herein.

Imported services shall be taxed upon rendering such services to service recipients in Egypt regardless of service rendering method. Tax shall not be due on transient goods, provided that such goods are transported under control of Customs Authority in accordance with the rules stipulated in the customs law.

Using, benefiting from, disposing of a commodity or a service by taxable persons for personal consumption or special use in any legal manner shall be deemed as a sale.

ARTICLE (6)

Goods and services exported abroad by free zones, cities and markets shall be zero-rated.

Goods and services supplied to such projects for carrying out related authorized business operations within the free zones, cities and markets except for passenger cars shall be zero-rated.

ARTICLE (7)

Without prejudice to the provisions of the second paragraph of Article (6) herein, VAT shall be chargeable on taxable goods or services in accordance with the provisions hereto for local consumption inside the free zones, cities and markets.

Importation for the sake of trading within free zone including a whole city shall be deemed as local consumption.

Importation made for commercial purposes within free zones that represent an entire city shall be deemed local consumption.

Tax is also due on imported taxable commodities or services in accordance with the provisions thereof from free zones, cities and markets to the local market inside the country.

Services and commodities manufactured in projects of free zones and cities shall be treated as imported from abroad when withdrawn for local consumption or use.

The Executive Regulations shall specify the limitations and rules governing the provisions of this article and Article (6) herein.

ARTICLE (8)

In case of suspension and/or liquidation of a business related to a taxable commodity or service, VAT shall be chargeable on commodities in the possession of registrants at the time of disposal unless the successor of the registrant is or shall be registered in accordance with the present law.

ARTICLE (9)

Without prejudice to the penalties stipulated herein, smuggled goods sales and sales made contrary to rules stipulated by laws shall be subject to tax rates effective on the date of crime or offense. In case the date is impossible to define, such sales shall be subject to the effective tax rates at the time of seizure or detection of the offense.

Chapter II Value

ARTICLE (10)

1. The value to be declared in the tax return that shall be taken as a basis of VAT assessment for taxable goods sold and services provided, even imported, shall be the amount actually paid or payable in any form of payment in accordance with the natural course of events.

2. In accordance with the provisions of the first paragraph of this article, the value to be declared in the tax return shall include the following:

a) Amounts collected from the purchaser or the service recipient under any name as long as such amounts are related to commodity sale or service provision; and

b) All incidental expenses, such as the costs of commission, packaging, sorting, transportation, insurance, charged by the seller on the purchaser and/ or importer.

3. Upon sale of a local or imported commodity or service between related persons, the value of sale shall not be less than the price applied between non-related persons as per market forces and transaction conditions.

4. In case of sales by bartering, the commodity value taken as a basis for VAT assessment shall be the sale price according to market forces and transaction conditions.

5. Value to be declared in the tax return for goods and services used for special usage shall be determined based on the total cost. Value of goods and services used for personal consumption shall be determined according to market forces and transaction conditions.

6. The value for installment sales taken as a basis of VAT assessment shall include the installment sale interest that exceeds the credit and discount rate declared by the Central Bank of Egypt (CBE) on the selling date. The Executive Regulations shall specify the rules and procedures of installment sale.

7. According to item (8) of this Article, value of imported goods shall be estimated upon the Customs release based on the value taken as a basis for Customs duty assessment including services relevant to the imported commodity in addition to Customs duty and any other taxes or duties levied, provided that the value to be declared upon sale in the local market shall not be less than value deemed a basis for tax assessment upon Customs release, unless there are commercial reasons justifying such reduced value. The Executive Regulations shall specify the reasons deemed commercial.

8. Tax base for goods and services imported from free zones and cities shall be the total value of the goods inclusive of the value of foreign and local components along with Customs duties and any other taxes or duties collected thereon.

9. The value taken as a basis for Tax assessment on sale of platinum, golden, silver and precious stoned jewelry shall be the value of manufacturing. The tax base for imported jewelry upon customs release shall be the value of manufacturing specified by the Customs Authority in addition to customs duty and other taxes and chargeable duties. Executive Regulations shall specify the stones deemed precious as well as the rules for calculating manufacturing value.

10. The value taken as a basis for tax assessment on sales of goods and services listed in Table attached hereto shall be as follows:

First: Sales of local goods and services:

The tax base shall be the value actually paid or payable in any form of payment in accordance with the natural course of events, in addition to the Table Tax.

Second: Imported goods and services:

a) Imported Goods: the tax base shall be the value taken as a basis for Customs duties assessment in addition to the Customs duties and any other levied taxes and duties as well as the Table Tax.

b) Imported Services: the tax base shall be the value actually paid or payable in any form of payment in accordance with the natural course of events in addition to Table Tax.

11. The value taken as a basis for tax assessment on new goods purchased by the registrant and re- sold after local use for at least two (2) years shall be 30% of the sale value without applying the provisions of discount stipulated in Article (22) herein upon sale.

12. The Minister of Finance may, in agreement with the Minister concerned, issue price lists of some goods and services, or establish accounting standards for the assessment of Tax.

ARTICLE (11)

The value of VAT shall be added to the price of goods or services including officially price- imposed and profit-fixed goods and services.

Prices of contracts concluded by two or more taxable parties, or among parties one of whom is a taxable person and which are prevailing at the time of charging VAT and Table Tax, or when amending tax brackets with the same amount or amending the tax burden shall be amended.

The Executive Regulations shall specify the rules for applying the second paragraph of this Article.

Chapter III Invoices, Returns, Notifications, Books and Records

ARTICLE (12)

Repealed(6)

(6) Article (12) was repealed by Law No. (206) of 2020 - Official Gazette - Edition (42 bis C) issued on October 19, 2020; and it used to read as follows:

ARTICLE (12)

Registrants shall issue a tax invoice upon sale of goods or services subject to VAT specifying the buyer's name and seller's registration number, if registered. The Executive Regulations shall specify the rules and procedures that ensure regular issuance, control and auditing of invoices.

The Minister of Finance may introduce a simplified system for VAT and Table Tax assessment for enterprises unable to issue tax invoices on each and every sale.

The Minister of Finance or the person so authorized may, in some cases, oblige the registrant not to issue any invoices of goods or services taxable to VAT or Table Tax, unless the invoices are approved by ETA.

ARTICLE (13)

Repealed(7)

(7) Article (13) was repealed Law No. (206) of 2020 - Official Gazette - Edition (42 bis C) issued on October 19, 2020; and it used to read as follows:

ARTICLE (13)

Registrants shall keep regular accounting books and records to manually or electronically record all transactions simultaneously, and shall keep such books, records and documents as well as copies of invoices for five years as of the end of the relevant fiscal year in which the entries were made in these books and records.

The Executive Regulations shall specify the limitations, rules and procedures as well as records and books the registrant shall manually and electronically keep, in addition to data to be recorded therein and documents to be kept.

ARTICLE (14)

*(8)

ETA has the right to assess tax for such tax period in which no tax return was not filed by registrant stating basis on which such assessment was built.

(8) Article (14) was repealed by Law No. (206) of 2020 - Official Gazette - Edition (42 bis C) issued on October 19, 2020; and then was added by law No. 3 of 2022 - Official Gazette - Edition (3 bis E) issued on January 26, 2022 .

ARTICLE (15)

*(9)

In case ETA amends such tax return after the first three years as of the elapse of the specified filing period, ETA may not charge the additional tax for the period following the elapsed three (3) years and until the registrant is notified of such amendment.

(9) Article (15, except paragraph 2) was repealed by Law No. (206) of 2020 - Official Gazette - Edition (42 bis C) issued on October 19, 2020; and it used to read as follows:

(Article 15 except paragraph 2)

In case the amount of tax due to be declared is different from the declared tax amount in the tax return for any tax period, ETA shall amend such tax return within five (5) years as of the elapse of the period specified for filing the tax return on such tax period according to Article (14) herein.

ETA shall notify the registrant of such amendment as well as the bases upon which the amendment was made using the form prepared for this purpose via certified mail or through any electronic means as per the Law of Electronic Signature or through any other written means by virtue of which ascertained knowledge is established.

The person concerned may, in all cases, appeal the assessment of ETA in accordance with the procedures stipulated herein.

Chapter IV Registration

ARTICLE (16)

*(10)

Every natural or judicial person who sells a taxable commodity or provides a taxable service, and whose total sales of taxable and exempt goods and services during the preceding 12 months as of date of enforcement of this law reach or exceed 500,000 Egyptian Pounds, shall apply to ETA to register their names and data on the form specified for such purpose within thirty (30) days as of the date his total sales reached registration threshold. Any person whose sales reach registration threshold after the enforcement date of the law in any fiscal year or part thereof shall apply for registration as mentioned herein. Natural persons who do not sell goods or provide services are not obliged to register in case their sales reached the abovementioned threshold.

Importer of a taxable commodity or service for the purpose of trading, exporters or distribution agents shall apply to ETA for registration regardless of their transaction volume..

The abovementioned registration threshold may be amended by virtue of a Ministerial decree.

(10) 3rd and 4th paragraphs od Article (16) were repealed by Law No. (206) of 2020 - Official Gazette - Edition (42 bis C) issued on October 19, 2020; and it used to read as follows:

(Article 16, 3rd and 4th paragraphs)

ETA shall notify the taxable person within the fourteen (14) days following the date of the registration request. Such person shall be subject to the provisions stipulated herein as of registration date.

In case the taxable person fails to apply for registration, such person shall be deemed registered by the force of law and shall be subject to the provisions of said law as of date the amount of their sales and services reach the registration threshold without prejudice to provisions of Article (68) herein.

ARTICLE (17)

*(11)

Every non-resident person who is not registered in ETA and sells taxable goods or provides taxable services to a non-registered person inside the country and who does not practice business through a permanent establishment in Egypt, shall apply for registration according to such simplified supplier registration system set forth in the Executive Regulations.

Legal persons who are not selling taxable goods or providing taxable services but are liable to assess tax on imported services according to paragraph (2) of article (23) hereof ,shall file an application to ETA for registration for the purposes of reverse charge system.

Provisions of this article hall apply to services for six months as of date of enforcement of simplified supplier registration system stipulated for in first paragraph of this article and shall apply to goods for a period of time not exceeding 2 years as of date of enforcement of such system.

(11) Article (17) was replaced by Law No. (3) of 2020 - Official Gazette - Edition (3 bis E) issued on January 26, 2022 .

ARTICLE (18)

The natural or juridical person who does not reach the registration threshold may apply to ETA to register their names and data in accordance with the terms, conditions and procedures specified by the Executive Regulations. Upon registration, such persons shall be deemed registrants governed by this law.

ARTICLE (19)

Repealed(12)

(12) Article (19) was repealed by Law No. (206) of 2020 - Official Gazette - Edition (42 bis C) issued on October 19, 2020; and it used to read as follows:

Article (19)

ETA shall keep a log in which the data of registration applications are recorded after reviewing and verifying such information and giving every registrant a certificate of registration.

The executive regulation shall specify the terms and conditions as well as rules and procedures on the registration certificates and the data included therein.

ARTICLE (20)

Repealed(13)

(13) Article (20) was repealed by Law No. (206) of 2020 - Official Gazette - Edition (42 bis C) issued on October 19, 2020; and it used to read as follows:

Article (20)

Every registrant shall in writing notify ETA of any changes made to the data previously presented in the registration application within twenty- one (21) days of such changes.

ARTICLE (21)

The Commissioner of ETA may deregister any registrant in some cases in accordance with terms and conditions stipulated in the Executive Regulations.

Chapter V Tax Deduction, Exemption and Refund

ARTICLE (22)

In accordance with limits, terms and conditions specified by the Executive Regulations, the registrant may, upon calculating the tax, deduct the tax previously paid or charged on their returned sales and inputs as well as goods sold by same registrant out of the tax due on their sales of such goods, at all phases of distribution.

The provision of the first paragraph of this article shall apply to the following:

1. Sales of goods and services provided to organizations stipulated in Clause (VIII) and Article (23) of this law.

2. Sales of goods and services funded by grants exempted by law.

3. The deduction shall be within the limit of the due tax. The non-deductible amount shall be carried over to the consequent tax period until the full deduction is made.

The above mentioned deduction referred to in the first paragraph of this article does not apply to the following:

1. Table Tax on goods and services, whether taxable as they are or as inputs of taxable goods and services, unless otherwise provided by a special provision herein.

2. Input tax included in the cost.

3. Exempted goods and services.

4. Cases registered under simplified supplier registration system set forth in paragraph (1) of Article 17 hereof. (14)

(14) 4th paragraph of Article (17) was replaced by Law No. (3) of 2020 - Official Gazette - Edition (3 bis E) issued on January 26, 2022.

ARTICLE (23)

The following shall be exempted, observing reciprocity principle according to the data of the ministry of foreign affairs:

1. Items bought or imported for personal use for members of foreign non-honorary diplomatic and consular corps who are appointed and incorporated in the lists issued by Ministry of Foreign Affairs, as well as items bought or imported for personal use for spouses and minor children of such personnel.

2. Items bought or imported by non-honorary embassies, commissions, and consulates for official use except for food, spiritual drinks and tobacco.

Number of vehicles exempted according to items (1) and (2) shall be defined by one (1) car for personal uses, and five (5) vehicles for embassy or commission official use, and two (2) vehicles for consulates use. Moreover, Minister of Finance in agreement with the Minister of Foreign affairs may increase such numbers.

3. Items imported for personal use, provided such are inspected, including personal effects, furniture, household, appliances and one (1) used vehicle for every foreign employee working for diplomatic and consular missions who do not enjoy exemptions stipulated in item (1) above, provided that such items shall be imported within six (6) months as of the arrival of the said person who shall benefit from this exemption. Besides, the Minister of Finance in agreement with the Minister of Foreign affairs may extend this term of time.

The aforementioned exemptions shall be granted ,after approval of exemption request by head of the diplomatic and consular missions, as the case may be, and pursuant to the ratification of the Ministry of Foreign Affairs.

ARTICLE (24)

Exempt items as per the provisions of Article (23) herein, are prohibited to be used for purposes other than the purposes specified for exemptions within the five (5) years following the exemption before notifying ETA and paying due tax based on the condition and value of such items as well as the tax rate applicable on payment date, unless otherwise stipulated in respect of reciprocal principle.

The Executive Regulations shall define rules and procedures governing same.

ARTICLE (25)

Items imported for personal use of some dignitaries may be exempted by virtue of a decree issued by the Minister of Finance and in agreement with the Minister of Foreign Affairs for the sake of international courtesy.

ARTICLE (26)

The following items shall be exempted from tax according to the limitations, terms and conditions stipulated in the Executive Regulations:

1. Samples used for analysis purposes by government laboratories.

2. Personal effects and items imported degraded of any commercial use such as decorations, medals as well as sports and academic prizes.

3. Supplies imported from abroad, with no compensation for damage or loss in consignments previously supplied or rejected and for which full tax was collected provided that Customs Authority verifies such instances.

4. Personal luggage of passengers coming from abroad.

5. Items on which tax was previously paid and exported abroad then re-imported as they are, provided that the Customs Authority verifies this.

ARTICLE (27)

*(15)

Some goods may be exempted from tax, by virtue of a decree issued by the Minister of Finance in agreement with the competent Minister in the following two cases:

1. Grants, donations, and presents given to state administrative bodies or local administration units.

2. Imports for academic, educational and cultural purposes by academic, educational and scientific research institutes.

(15) Article (27) was replaced by Law No. (3) of 2020 - Official Gazette - Edition (3 bis E) issued on January 26, 2022.

Article (28)

Each and every goods, equipment ,machinery and services relevant to this law and necessary for the purposes of armament for national defense and security as well as material and supplies required for production and parts used in manufacturing thereof.

Article (28 bis)

*(16)

Payment of tax due on machinery and equipment imported from abroad or bought from local markets for factories and production units for use in manufacturing, shall be suspended for one year as of date of release or purchasing from local markets as the case may be. Such period of time may be extended for one more period or periods of time no later than a maximum of one year based on justifiable reasons accepted by ETA. If proved to ETA that such machinery and equipment are used in manufacturing during such period of time , same shall be exempted from such tax due referred to. In such case , disposal of such machinery and equipment shall be banned if used for purposes other than those for which they were exempted for such five years following exemption before notifying ETA and payment of tax due according to status , value, and thereof as well as tax rate applicable on date of payment.

Upon elapse of such period of time referred to in paragraph (1) of this article without use of such machinery and equipment in industrial production, tax shall be payable as of date of customs release of such machinery and equipment or purchase of such from local market as the case may be until date of payment.

Executive Regulations shall define rules and procedures regulating this.

(16) Article (28 bis) was added by Law No. (3) of 2020 - Official Gazette - Edition (3 bis E) issued on January 26, 2022.

ARTICLE (29)

Without prejudice to the provision of Clause (VIII), other tax exemptions stipulated in other laws or decrees shall not apply to this tax unless this exemption is explicitly stipulated.

ARTICLE (30)

*(17)

VAT shall be refunded, according to the conditions and procedures and within the limits specified by the Executive Regulations, within forty-five (45) days as of the date of submitting the application supported by documents in the following cases:

1. Tax previously paid or charged on exported goods or services whether in same condition or included in other goods or services but not exceeding the credit balance, provided that the value of exports shall be supplied to a bank subject to the supervision of the Central Bank of Egypt (CBE) and according to rules provided by the Central Bank of Egypt (CBE) or according to any of the payment methods or other settlements stipulated by the Executive Regulations, provided that the value of exports shall not be less than the value of their inputs.

2. Tax collected by mistake.

3. Credit balance which lasted for more than six (6) successive tax periods.

4. Tax previously paid on machines and equipment used in the production of a taxable commodity or in providing a taxable service upon filing of the first tax return except for buses or passenger cars, unless the usage of such is the licensed activity of the enterprise.

5. Tax paid by non- resident registrant according to simplified supplier registration system to nationally do business.

In all cases, a report signed by an auditor registered in the Accountants and Auditors Table shall be submitted with other documents supporting the right of the taxable person to tax deduction or refund unless tax was proved to be electronically paid to ETA.

(17) Article (30) was replaced by Law No. (3) of 2020 - Official Gazette - Edition (3 bis E) issued on January 26, 2022.

Article (30 bis)

*(18)

Foreign visitors upon departure from Egypt have the right ,no later than three months ,to refund tax previously paid to registered seller as to taxable purchases provided that amount of each and every invoice is not less than EGP 1500 and that purchases are in his possession or in any other means upon departure from Egypt. Executive Regulations shall set rules governing application of such article.

(18) Article (30 bis) was added by Law No. (3) of 2020 - Official Gazette - Edition (3 bis E) issued on January 26, 2022.

Chapter VI Tax Collection

ARTICLE (31)

*(19)

Ministries, government entities and agencies, municipal units and public agencies and other public legal persons shall directly remit table tax due to ETA within ten days as of date of tax being payable. Such entities and agencies shall directly remit 20% of VAT due to ETA within same period of time previously referred to as part of total amount of tax withheld thereby. ETA may not request taxable persons to collect amounts previously been remitted and all this shall be set forth in Executive Regulations.

Tax on imported goods shall be paid upon release by Customs Authority according to procedures set for payment of customs duties. Such goods may not be finally released before full payment of tax due unless it was proved that non- resident registrant has collected tax on imported goods being released by Customs.

Without prejudice to provisions of Article (28bis ) herein, Commissioner or whoever duly delegated by him may, for three months, temporarily release consignments imported for production process or doing business based on guarantees that Customs Authority finds suitable until concerned person submits required documents to Authority to verify qualification to exemption within such stated period of time or payment of tax due and additional tax assessed as of date of consignment release.

(19) Article (31) was replaced by Law No. (3) of 2020 - Official Gazette - Edition (3 bis E) issued on January 26, 2022.

ARTICLE (32)

*(20)

In case a non-resident who is not registered in ETA sells a service in Egypt to a registered person, governmental organization, public or economic agency or any other agency where such services are not essential for doing their business operations, the beneficiary of such service shall calculate and pay the due tax to ETA within thirty (30) days as of selling date, unless such non-resident is registered in the streamlined supplier registration system.

Legal persons subject to reverse charge system referred to in second item of article ( 17) herein and import services shall assess tax due on such services and pay such tax to ETA within 30 days as of date of supplying such service unless such non-resident non registrant person is registered in the streamlined supplier registration system.

(20) Article (32) was replaced by Law No. (3) of 2020 - Official Gazette - Edition (3 bis E) issued on January 26, 2022.

ARTICLE (33)

Issuance of invoice by service provider is the tax incidence according to the provisions stipulated herein concerning services of a continuous nature. The Executive Regulations shall define such services.

ARTICLE (34)

Repealed(21)

(21) Article (34) was repealed by Law No. (206) of 2020 - Official Gazette - Edition (42 bis C) issued on October 19, 2020; and it used to read as follows:

(Article 34)

Collecting tax and any other due amounts according to the provisions specified herein shall follow the provisions of law No. (308) of the year 1955 on administrative seizure as well as the provisions and procedures stipulated herein.

The provisions of the first paragraph of this article are applicable to companies and enterprises regardless of legal system thereof.

ARTICLE (35)

Repealed(22)

(22) Article (35) was repealed by Law No. (206) of 2020 - Official Gazette - Edition (42 bis C) issued on October 19, 2020; and it used to read as follows:

(Article 35)

Offset shall be made by force of law of the entitlements of registrant and due liabilities by any tax law applied by ETA or any other revenue authority affiliated to the Ministry of Finance.

Section III Table Tax

ARTICLE (36)

Table Tax shall be charged for selling, providing or importing goods and services stipulated in the attached table hereto. Table Tax rate shall be according to percentages and values of goods and services stipulated in the table in addition to the tax stipulated in Article (2) herein.

Table Tax shall be charged at zero rate on goods and services that shall be exported in accordance with the terms and conditions specified by the Executive Regulations.

Table Tax shall not be recharged unless a change occurs to the commodity status. Packaging, repackaging, refining, purification or grinding is not deemed a change in the commodity status without prejudice to charging the tax on goods and services stipulated in the attached table, unless otherwise stipulated in the table.

ARTICLE (37)

The registrant has the right to settle the tax previously paid on parts of machines and equipment as well as spare parts used in manufacturing Table Tax taxable goods and services, against the value of the Table Tax and only within the limit of the due amount of Table Tax until the depletion of same.

The registrant has the right to settle the Table Tax previously paid on the sales’ returns of same against due Table Tax and in accordance with the terms and conditions stipulated in the Executive Regulations.

ARTICLE (38)

The Table Tax on goods and services stipulated in the attached table shall be charged only once at the point of sale of goods or provision of service for the first time or upon the importation of goods or service, without prejudice to charging the tax stipulated in Section II herein.

The provision of the first paragraph of this article shall apply to goods and services stipulated in the attached table upon disposal of such in the form of free-of-charge goods and services or promotions. The value of goods and service shall, in this case, be determined as per the market forces and transaction conditions. The Executive Regulations shall define promotions.

ARTICLE (39)

The amount to be declared and taken as a basis of Table Tax for goods or services stipulated in the attached table shall be as follows:

(A) for local goods and services:

The basis shall be the amount actually paid or payable in any form of payment according to the natural course of events.

(B) for imported goods and services:

The basis shall be the amount taken as a basis for customs duty in addition to the customs duty and any other imposed taxes and duties.

Unless otherwise stipulated in the attached table.

ARTICLE (40)

In case a commodity or service is taxable according to the Table Tax or the tax rate of such tax is increased, the importers, wholesalers, traders, retailers, and distributors shall submit to ETA a list of inventory of such goods and services on the day preceding the date of applying the new or increased Table Tax. Such inventory list shall be submitted to the ETA within fifteen (15) days as of this date. The new or increased Table Tax shall be charged on the date of submitting the inventory list. The Table Tax on such goods and services shall be paid within the period specified by the Commissioner of ETA, provided that such period does not exceed six (6) months as of due date of such tax.

ARTICLE (41)

Each producer, service provider or importer of goods and services stipulated in the attached table herein shall be registered at ETA regardless of the volume of sales or production as per the rules and procedures stipulated by the Executive Regulations.

ARTICLE (42)

Any plant or laboratory for producing any commodity or rendering any services stipulated in the table attached herein may only be established or operated after obtaining a license from the administrative body concerned in accordance with the terms and conditions specified by the competent Minister along with the Minister of Finance.

Every manufacturer of such goods or provider of such services shall, in case of whole or partial suspension of the operations of business of the plant, laboratory or headquarters through which the activity is carried out for any reason, notify ETA. Also, ETA should be promptly notified upon the discontinuance of suspension period as prescribed by the Commissioner of ETA.

ARTICLE (43)

The provisions of the present law shall apply to goods and services enumerated in the attached table herein, unless otherwise prescribed by a special provision in this section and the attached table.

Section IV General Provisions, Control and Appeal Procedures

Chapter I General Provisions

ARTICLE (44)

Without prejudice to any special provision prescribed herein, it is prohibited to dispose of any goods exempted from VAT or Table Tax, or to use such goods in purpose other than the purposes for which such goods are exempted within five (5) years following the exemption except after notifying ETA and paying the due tax according to the value of goods and applicable tax rate at the date of disposal.

Prohibition stipulated in the first paragraph of this article shall apply to machines and equipment for which tax is previously refunded in accordance with item (4) of article (30) herein.

Due tax must not, in all cases, exceed the amount of the tax previously exempted or refunded.

ARTICLE (45)

ETA may, when necessary, take samples of some goods to be analyzed and may consult any experts deemed necessary.

The person concerned may ask for repeating the analysis on his own expense. The Minister of Finance shall issue decree determining the methods and procedures of taking such samples.

ARTICLE (46)

Executive Regulations shall determine the amounts charged by ETA as prices of printed materials, banderole stamps, special marks as well as stamping, analysis expenses and other services provided by ETA officers as well as labor fees for working overtime at times other than the official working hours for the sake of persons concerned.

Such amounts are not included under any exemption or refund of VAT or Table Tax stipulated herein.

ARTICLE (47)

Without prejudice to the provisions of the Customs Law, ETA may dispose of the seizures and smuggling tools as well as means of transportation confiscated in accordance with the rules specified by the Executive Regulations.

ETA may, by a judicial order and before issuance of a ruling, dispose of the seizures subject to damage, decrease or loss and has, after consulting the competent technical authorities, the right to destroy prohibited goods or harmful goods that threaten public health or goods that may jeopardize the security and safety of citizens.

ARTICLE (48)

Repealed(23)

(23) Article (48) was repealed by Law No. (206) of 2020 - Official Gazette - Edition (42 bis C) issued on October 19, 2020; and it used to read as follows:

(Article 48)

ETA may, in all cases, assess VAT or Table Tax and/or amend the tax return filed by registrants only based on in-hand available data or documents within five (5) years as of the elapse of the period legally specified for filing the return on such tax period. Such period shall be six (6) years in case the registrant commits tax evasion.

The period shall be interrupted by any form of prescription intervals stipulated in the Civil Law, or through notifying the registrant of the tax assessment and payment, or by referral to appeal committees.

ARTICLE (49)

Taxable imported goods unreleased from Customs shall be subject to the provisions of violations and evasions set forth in Customs Law.

ARTICLE (50)

*(24)

Taxable person shall pay an amount equivalent to (1%) of amount of tax and table tax due not less than one thousand pounds and does exceed ten thousand pounds in addition to tax,table tax and additional tax due in case of violation of provisions ,procedures,and systems set forth herein and without considering such violation as any such act of evasion stipulated for herein.

The following cases shall be deemed violations hereof:

1- A deficit or surplus in goods deposited in free zones and markets in violation of provisions of Customs Law.

2- Failing,on date set to notify ETA of such changes that may be introduced to data listed in the registration application.

3- Violation of provisions ,procedures or systems set forth herein.

Amount of fine shall be doubled in case committing such act within three years.

(24) Article (50) was repealed Law No. (206) of 2020 - Official Gazette - Edition (42 bis C) issued on October 19, 2020 ; and then added by Law No. (3) of 2022 - official Gazette - Edition (3 bis E) issued on January 15, 2022.

ARTICLE (51)

Repealed(25)

(25) Article (51) was repealed by Law No. (206) of 2020 - Official Gazette - Edition (42 bis C) issued on October 19, 2020; and it used to read as follows:

(Article 51)

VAT, Table Tax, additional tax and any other amounts due to ETA, by virtue of the present law, has the priority over all other debts or money, except for the judicial expenses, of tax debtors or taxable persons who are assigned by force of law to collect and remit tax to ETA.

Chapter II Control

ARTICLE (52)

Executive Regulations shall define the required control systems over the registrant books and records as well as IT systems and electronic sale machines used by registrants for selling goods, providing services or importing service taxable to VAT or Table Tax in order to verify compliance of registrants to calculate such taxes as per the present law.

The Minister or the person so authorized may decide the procedural provisions and rules required to apply the provision of the present law according to the business operations of some registrants.

ARTICLE (53)

Repealed(26)

(26) Article (53) was repealed by Law No. (206) of 2020 - Official Gazette - Edition (42 bis C) issued on October 19, 2020; and it used to read as follows:

(Article 53)

The Minister may establish one or more systems that enable ETA to electronically receive tax returns, copies or data of tax invoices issued by or for the registrant. The registrant shall present the invoice copies or data and receipts of cash register machines to ETA upon request according to such system.

The Minister or the person so authorized may oblige all or some enterprises to use cash register machines that declare the amount of sales or supplies and the due tax thereof.

ARTICLE (54)

Any transaction the main purpose(s) thereof is to avoid compliance, deferral, or reducing the burden of VAT and Table Tax shall not be taken into consideration. In the application of this article, the following shall be deemed tax avoidance:

1. transactions among related enterprises in terms of selling goods and services subject to VAT or Table Tax, where the objective thereof is to avoid reaching the legally set registration threshold for one or more of such enterprises.

2. Setting up or division of enterprises or breaking down transactions thereof for tax purposes.

In case the transaction is deemed as tax avoidance, ETA has the right to oblige the taxable person to register or pay the tax based on the actual value according to market conditions and transaction forces. That is without prejudice to the right of taxable persons to prove that the transaction is carried out for purposes other than tax avoidance.

One committee or more shall be formed and chaired by the Commissioner of ETA or the person so authorized in addition to members from ETA staff who at least assume the position of a general manager. The committee shall be responsible for considering avoidance cases and committee decisions shall be binding to tax office concerned.

Chapter III Appeal Procedures

ARTICLES (From 55 To 61)

All Repealed(27)

(27) Chapter III of Section (4) except for Article (62) were repealed by Law No. (206) of 2020 - Official Gazette - Edition (42 bis C) issued on October 19, 2020; and such articles used to read as follows:

Article (55)

The notification sent via a certified mail or through any electronic means for which in pursuance of the Law of Electronic Signature no. 15 of the year 2004 shall be determined by a Ministerial decree that shall be legally authentic and shall have the same effect as the notification using legal methods including notifying such person subjected to seizure procedures with a copy of the seizure report.

The notification shall be legally valid whether the registrant received the notification from the tax office or the appeal committee concerned or in the registrant enterprise premises or chosen domicile.

In case the enterprise is closed or the registrant is unavailable where it is difficult to be notified using one of the aforementioned notification methods or in case the registrant refuses to receive the notification, an ETA officer authorized to practice judicial seizure shall write a report on the incidence that shall be posted on the announcement board of the relevant tax office or appeal committee, as the case may be, as well as on the premises of the registrant enterprise.

In case the notification is sent back indicating that the enterprise does not exist or that the registrant address could not be found, the registrant shall be notified before the public prosecution after carrying out the necessary investigations.

The announcement made as well as the notification given as previously explained before the public prosecution shall be deemed a decisive procedure to avoid the statute of limitation.

In cases prescribed in the third and fourth paragraphs of this article, the registrant may appeal tax assessment decision taken by ETA or appeal committee decision, as the case may be, within sixty (60) days as of the date of seizure, otherwise the decision of tax assessment made by ETA or appeal committee decision shall be final.

ARTICLE (56)

In case of tax amendment or assessment by ETA, the registrant shall be notified via certified mail or through any electronic means as per the Law of Electronic Signature or through any other written means in virtue of which ascertained knowledge of such amendment or assessment is established.

Registrants may appeal such amendment or assessment within thirty (30) days as of date of notification of such tax amendment and/or assessment.

The appeal document of such tax amendment or assessment submitted by the registrant to the tax office shall be of three copies, one of which stamped with the submission date shall be delivered back to the registrant. The tax office records the appeal data and summary of any contained disputes in a special log.

ETA shall review the appeals through internal committees, whose formation, premises and jurisdiction are determined by a decision of the Commissioner of ETA, within sixty (60) days as of the submission date of appeal.

In case disputes are settled, the tax shall be final.

In case disputes are not settled, the tax office shall notify the registrant of such result, and shall refer the disputes to the appeal committee concerned within thirty (30) days as of the date of dispute resolution, provided that the tax office notifies the registrant of such referral via certified mail. Upon the elapse of the thirty-day period and in case the tax office did not refer the dispute to the appeal committee concerned, the registrant may present the matter in writing or via certified mail directly to the committee chairman within fifteen (15) days as of the elapse of the previously stipulated period. The committee chairman shall, within fifteen (15) days as of the date of presenting the case or receiving the certified mail, set a date for a session to consider the dispute and give orders to study the registrant file.

The procedures stipulated in this article may be carried out via any electronic means determined by the Minister.

Tax amendment or assessment by ETA shall be deemed final in case an appeal is not submitted during the aforementioned periods.

Executive Regulations shall govern the rules of the formation of internal committees and work procedures thereof and validate the agreements concluded before such committees.

ARTICLE (57)

Appeal committees shall be formed by virtue of a decree by the Minister or the person so authorized and be chaired by a chairman who is not from ETA staff. Each committee includes two ETA members selected by the Minister or the person so authorized, and two experts nominated by the syndicate of commercial professionals who are registered in the list of accountants and auditors for corporations in the public register of freelance profession of accounting and auditing.

The Minister or the person so authorized may appoint alternate members to ETA staff members in such committees in cities with only one committee. The original members shall be deemed backup members for other committees in cities with more than one committee. Secondment of such members instead of the committee original members who fail to attend the committee sessions shall be the jurisdiction of the chairman of the original committee or the oldest committee member upon the absence of the chairman.

Committee sessions shall not be legally concluded unless the chairman and at least three members attend. The secretary of the committee shall be an employee seconded by ETA.

Appeal committees shall be permanent and shall be reporting directly to the Minister. The formation of such committees, premises, jurisdiction and compensations for committee members shall be decided by the Minister or the person so authorized.

ARTICLE (58)

Appeal committees shall resolve all disagreements between registrants and ETA on disputes related to taxes stipulated herein.

The committee shall notify both the registrant and ETA of the appeal session at least ten (10) days prior to session date via certified mail. The committee may ask both the registrant and ETA to present all necessary data and documents. The registrant shall attend before the committee by himself or by a representative; otherwise the committee shall resolve the appeal as per the submitted documents.

The committee shall issue its decision taking into consideration ETA assessment and the registrant requests. The tax assessment shall be amended according to the committee decision. In case VAT has not been collected yet, tax shall be collected by virtue of such decision.

ARTICLE (59)

Sessions of appeal committees shall be confidential and shall take justifiable decisions with the majority of the attending members. In case of equal votes the committee decision shall be in favor of the chairman’s side of voters. Decisions shall be signed by the committee chairman and secretary within a period not exceeding fifteen (15) days as of the issuance of decisions.

The committee shall observe the general rules and principles of litigation procedures. Both the registrant and ETA shall be notified of the committee decision via certified mail. The tax shall be payable based on the decision of the appeal committee. Challenging the decision of the appeal committee before the administrative court will not prevent tax collection.

ARTICLE (60)

Both the registrant and ETA may challenge the decision of the appeal committee before the court concerned within sixty (60) days as of the announcement date of the decision.

ARTICLE (61)

The court may consider lawsuits brought by or against the registrant in a confidential session in which the court ruling shall be made promptly.

ARTICLE (62)

Arbitration provisions and procedures stipulated in the Customs Law shall be applied to imported goods and services under the control of the Customs Authority.

Chapter IV ETA Employees and Respective Obligations

ARTICLE (63)

*(28)

For purposes of executing such work and by a virtue of a written permission from the Commissioner of ETA or any person so authorized, ETA employees shall inspect laboratories, plants, warehouses, shops and enterprises of business in taxable goods or services and in case of seizure, officials from other authorities may, if necessary, be utilized.

(28) 1st paragraph of article (63) was repealed by Law No. (206) of 2020 - Official Gazette - Edition (42 bis C) issued on October 19, 2020; and such articles used to read as follows:

(1st paragraph of article 63)

ETA employees whose positions are determined by virtue of a decree issued by Minister of Justice in agreement with the Minister of Finance shall have the powers of judicial officers in the application of the provision hereof and in implementing decisions thereof.

Article (64)

*(29)

ETA employees, who have the powers of judicial officers have the right to access and seize papers, documents, books, records and invoices regardless of type, related to the application of the provisions of this law, upon finding evidence proving violation of the provisions thereof.

Such employees may, by virtue of a written permission from the Commissioner of ETA or any person so authorized, take specific samples of goods for purposes of analysis or examination.

(29) Article (64) except 1st and 2nd paragraphs were repealed by Law No. (206) of 2020 - Official Gazette - Edition (42 bis C) issued on October 19, 2020; and such articles used to read as follows:

(Article 64 except 1st and 2nd paragraphs)

Every person who, in their professional capacity and/or jurisdiction, has the authority to assess, charge or collect taxes stipulated herein or to settle disputes related to such taxes, shall be obligated to observe the profession confidentiality.

ETA staff whose job is not directly related to assess, charge or collect taxes may not provide any data, or give access to any papers, statements, files or other types of data to third parties unless only in legally such data is authorized for provision to third parties.

ETA staff may not provide any data included in tax files unless upon a written request by the registrant or by virtue of a provision of any other law.

Giving information to successors of registrants referred to in Article (8) herein, or exchange of information and data among revenue authorities affiliated to the MOF in accordance with the organization made by a ministerial decree is not considered a disclosure of confidentiality.

ARTICLE (65)

In cases other than being caught red-handed, no investigation procedures may be triggered against ETA employees who have the capacity of judicial seizure during the course of or due to performing work unless such investigation procedures are taken by virtue of a written request from the Minister or any person so authorized.

In all cases no criminal action may be filed against such employees until obtaining such request.

Section V Crimes and Penalties

ARTICLE (66)

Repealed(30)

(30) Article (66) was repealed by Law No. (206) of 2020 - Official Gazette - Edition (42 bis C) issued on October 19, 2020; and such articles used to read as follows:

(Article 66)

With the exception of tax evasion actions set forth herein, violations of provisions, procedures, or rules prescribed in this law and the Executive Regulations thereof shall be penalized with a fine not less than five hundred (500) Egyptian Pounds and not exceeding five thousand (5000) Egyptian Pounds in addition to VAT, Table Tax and additional tax due.

The following cases shall be deemed violations of the provisions prescribed herein:

1. Delay not exceeding sixty (60) days in filing tax return and in paying due VAT and Table Tax for the period specified in Article (15) of this law.

2. Submission of false data regarding sales of taxable goods or services in case of discovering that actual sales are more than the amount stipulated in the return.

3. In case of discovering shortage or surplus in the goods deposited in free zones and free markets violating the provisions of Customs Law.

4. Failure to notify ETA of any change in the data included in the registration application on due date.

5. Obstructing ETA employees in performing respective duties or exercising respective jurisdictions in controlling, inspection, checking, reviewing, requesting or accessing documents.

The aforementioned penalty shall be doubled in case of recommitting same crime within three (3) years.

ARTICLE (67)

Without prejudice to any graver penalty prescribed in any other law, committing tax evasion related to VAT and Table Tax shall be penalized by imprisonment for a term of at least three (3) years and not exceeding five (5) years as well as a fine of at least five thousand (5.000) Egyptian Pounds and not exceeding fifty thousand (50.000) Egyptian Pounds or by one of the two aforementioned penalties.

Means of transportation, tools and materials used in tax evasion related to VAT or Table Tax, may be confiscated by virtue of a ruling except for ships and aircrafts, unless such are actually prepared or rented by owners of such ships and aircrafts for such purpose.

Collaborative perpetrators shall, as the case may be, jointly pay VAT or Table Tax or both as well as additional tax.

The aforementioned penalty prescribed in the first paragraph of this article shall be doubled in case same crime is recommitted within three (3) years.

Evasion cases shall be reviewed promptly upon referral to courts.

Tax evasion of VAT and Table Tax shall, in all cases, be deemed an offense involving breach of honor and integrity.

Article (67bis)

*(31)

Without prejudice to penalties provided for herein or in any other law and in case of failure of non-resident registrants to fulfill obligations set herein, the Minister may request public prosecution to order ban or prevention of access to Egyptian markets until registrant fulfill such obligations and consequences thereof and relevant entities shall promptly enforce such order upon issuance.

(31) Article (67 bis) was added by Law No. (3) of 2022 - official Gazette - Edition (3 bis E) issued on January 26, 2022 .

ARTICLE (68)

The following cases shall be deemed tax evasion and shall be punishable by the penalties set forth in article (67):

1. Failure to apply to ETA for registration on due dates.

2. Sale or importation of commodity and/or provision or importation of service without declaring such in the tax return and without paying due VAT and Table Tax.

3. Wholly or partially deduct tax or Table Tax unduly violating provisions and limits of deduction.

4. Unlawfully and knowingly refunding whole or part of VAT or Table Tax.

5. Submitting false, forged or fabricated documents or records to evade paying VAT and Table Tax wholly or partially.

6. Failure by registrants to issue invoices on their sales of goods and services subject to VAT and Table Tax.

7. Repealed(32)

8. Issuance of invoices charged with tax and table tax by non-registrants.

9. Repealed(33)

10. Falsely issuing invoices to others without being duly relevant actual sales transactions and responsibility shall fall jointly on issuer of false invoice and beneficiary thereof.

11. Repealed(34)

12. Possession of taxable goods for trading in spite of knowing that such goods are smuggled.

13. Failures to file a final tax return and/or pay the total due tax by virtue of the present law within six (6) months as of the date of deregistration.

14. Failure to comply with the provisions of article (40) or article (42) of this law.

15. Placing fabricated marks and/or stamps to avoid paying Table Tax wholly or partially.

16. Producer, distributor or trader sells Table goods with for which the base of VAT and Table Tax is the consumer price with a price higher than that taken as the basis for calculating tax whether such is the declared price by producers or importers of such goods or the one enrolled in the price lists defined by the Minister, without paying the due tax on the increase of prices.

17. Possession of table goods for the purpose of trading without using a banderole sticker according to the instructions of the Minister.

18. Disposal of goods exempted from VAT and Table Tax in purposes other than the intended exemption purpose within the prohibition period without informing ETA or paying the due tax.

19. Failure to comply with the provisions of Clauses (IV) or (V).

(32) Items (7) of Article (68) was repealed by Law No. (206) of 2020 - Official Gazette - Edition (42 bis C) issued on October 19, 2020; and such articles used to read as follows:

(Item 7)

Elapse of 60 days as of dates set for payment of tax and table tax without declaration of and payment thereof.

(33) Items (9) of Article (68) was repealed by Law No. (206) of 2020 - Official Gazette - Edition (42 bis C) issued on October 19, 2020; and such articles used to read as follows:

(Item 9)

Failure to comply with rules, procedures and controls set to secure periodic issuance of invoices according to provisions of Article 12 herein.

(34) Items (11) of Article (68) was repealed by Law No. (206) of 2020 - Official Gazette - Edition (42 bis C) issued on October 19, 2020; and such articles used to read as follows:

(Item 11)

Failing to keep regular accounting books and records by registrant according to article 13 herein.

ARTICLE (69)

Without prejudice to the provisions of Article (67) herein, goods stipulated in the attached table herein subject to tax evasion shall be confiscated. In case of failing to seize such goods, the penalty shall be equivalent to the value thereof. Means of transportation, tools and materials used in smuggling may be confiscated except for ships and aircrafts, unless such are specifically prepared or rented for this purpose.

ARTICLE (70)

Repealed(35)

(35) Article (70) was repealed by Law No. (206) of 2020 - Official Gazette - Edition (42 bis C) issued on October 19, 2020; and such articles used to read as follows:

(Article 70)

In case of committing any tax evasion act by a judicial person, the person responsible for such act shall be managing partner, acting manager, managing director (CEO) or chairman of board of directors – whoever actually assumes the responsibility of management as the case may be.

ARTICLE (71)

Every accountant registered in the accountants and auditors list proved to be violating the compliance prescribed in the last paragraph of Article (30) herein shall be penalized by suspension from practicing the profession for a year and paying a fine of at least ten thousand (10.000) Egyptian Pounds and not exceeding fifty thousand (50.000) Egyptian Pounds. In case of recommitting same crime, the original penalty shall be applied.

ARTICLE (72)

Repealed(36)

(36) Article (72) was repealed by Law No. (206) of 2020 - Official Gazette - Edition (42 bis C) issued on October 19, 2020; and such articles used to read as follows:

(Article 72)

Filing a criminal case or taking any procedures regarding tax evasion and other crimes prescribed herein may not be carried out except at the request of the Minister or any person so authorized.

The Minister or any person so authorized may conciliate on the aforementioned tax evasion crimes before a final ruling on the criminal action is issued in compensation of payment of due VAT or Table Tax or both, as the case may be, as well as additional tax and compensation not exceeding half of the maximum amount of the fine prescribed in Article (66) in case conciliation is on a crime listed therein, in addition to a compensation equivalent to half of VAT or Table Tax or both, as the case may be, in case conciliation is on tax evasion crime. If, however, conciliation is on a crime prescribed in Article (71) herein, the compensation shall not be exceeding half of the maximum fine amount stipulated therein.

Conciliation on criminal actions shall directly result in canceling the criminal case as well as consequences thereof including any enforced penalty.

Section VI Closing Provisions

ARTICLE (73)

Repealed(37)

(37) Article (73) was repealed by Law No. (206) of 2020 - Official Gazette - Edition (42 bis C) issued on October 19, 2020; and such articles used to read as follows:

(Article 73)

The Minister shall, after consulting with the Prime Minister, introduce one or more incentive systems for rewarding ETA employees in accordance with their performance rates and work achievements.

ARTICLE (74)

The Minister shall upon the approval of the Council of Ministers implement a rewarding system to encourage dealing with tax invoices, provided that such system includes scopes, conditions and rules regulating implementation of such system. The reward may not exceed 1% of the annual tax collection. The Executive Regulations shall prescribe rules governing such rewarding system.

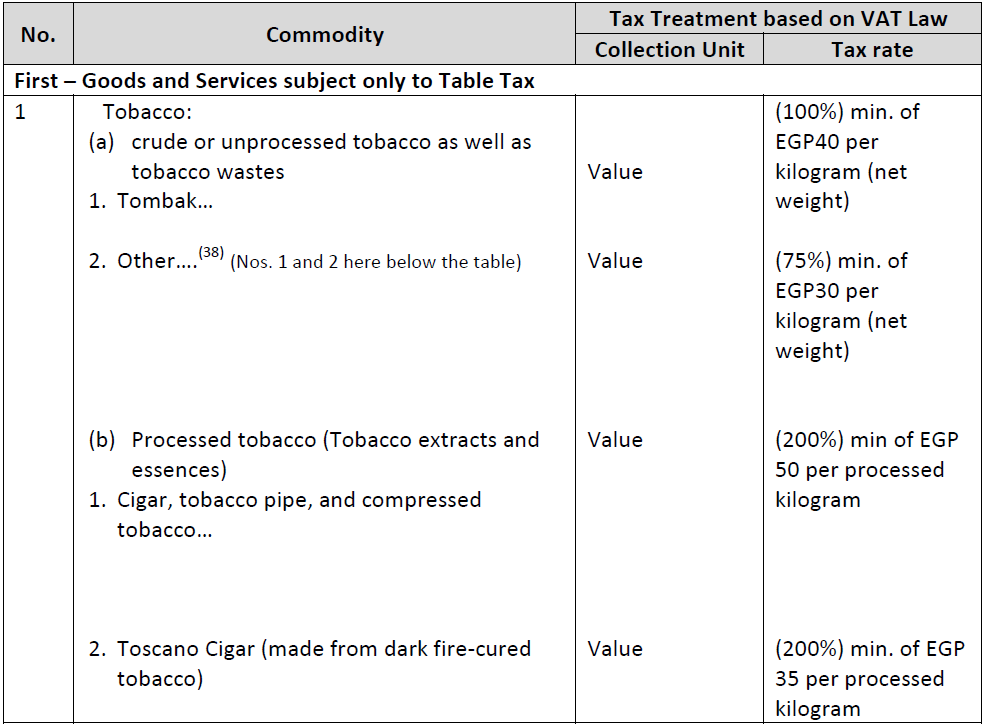

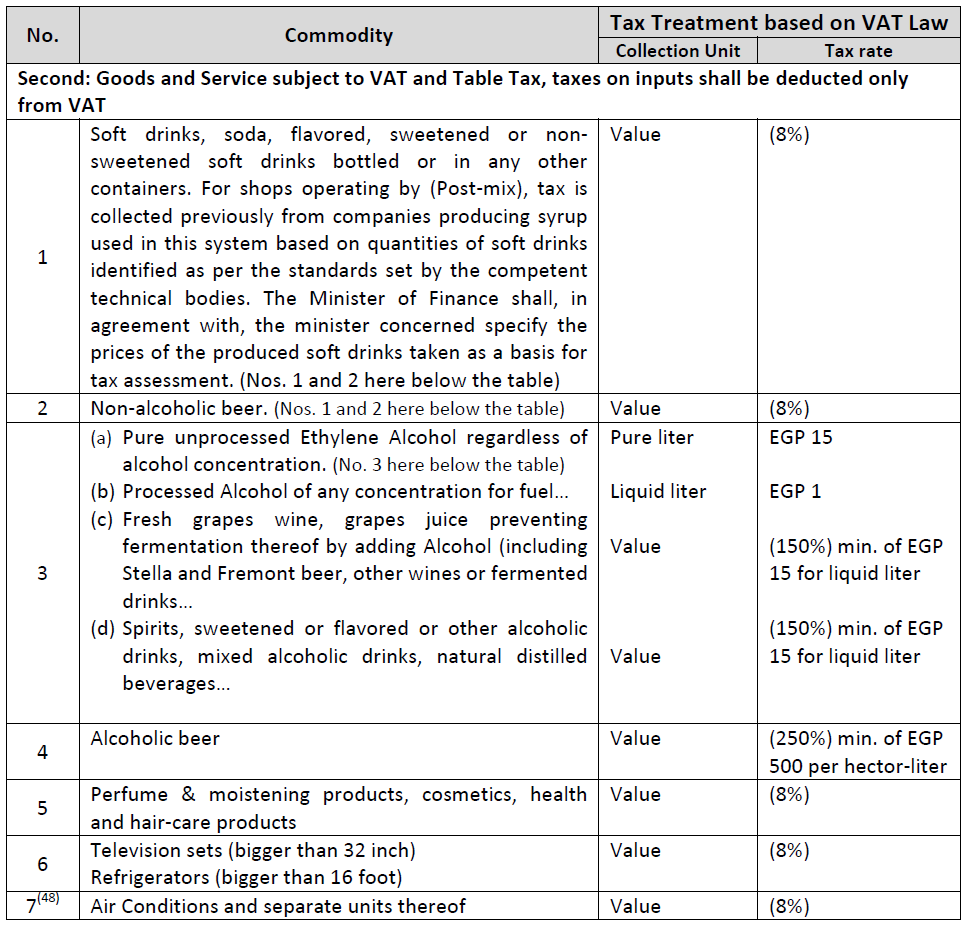

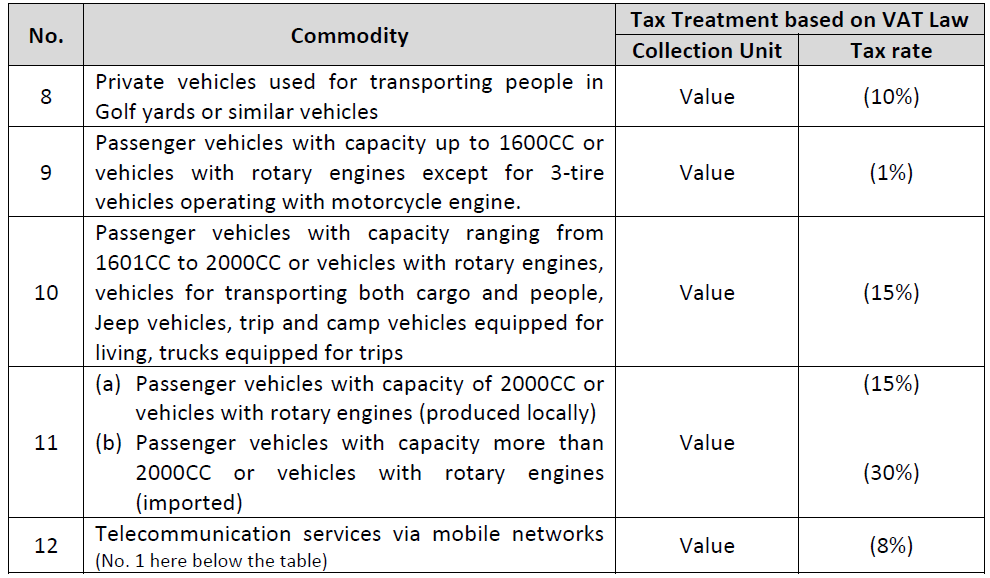

Goods and Service Table attached to the Value Added Tax (VAT) Law(*)

1) Importer shall notify ETA of agencies which purchased tobacco, and the manner of disposal of imported tobacco quantities within fifteen (15) days following the month of sale.

2) Table Tax collected on such item shall be settled, in case being one of the components of local product, against Table Tax due on such local product.

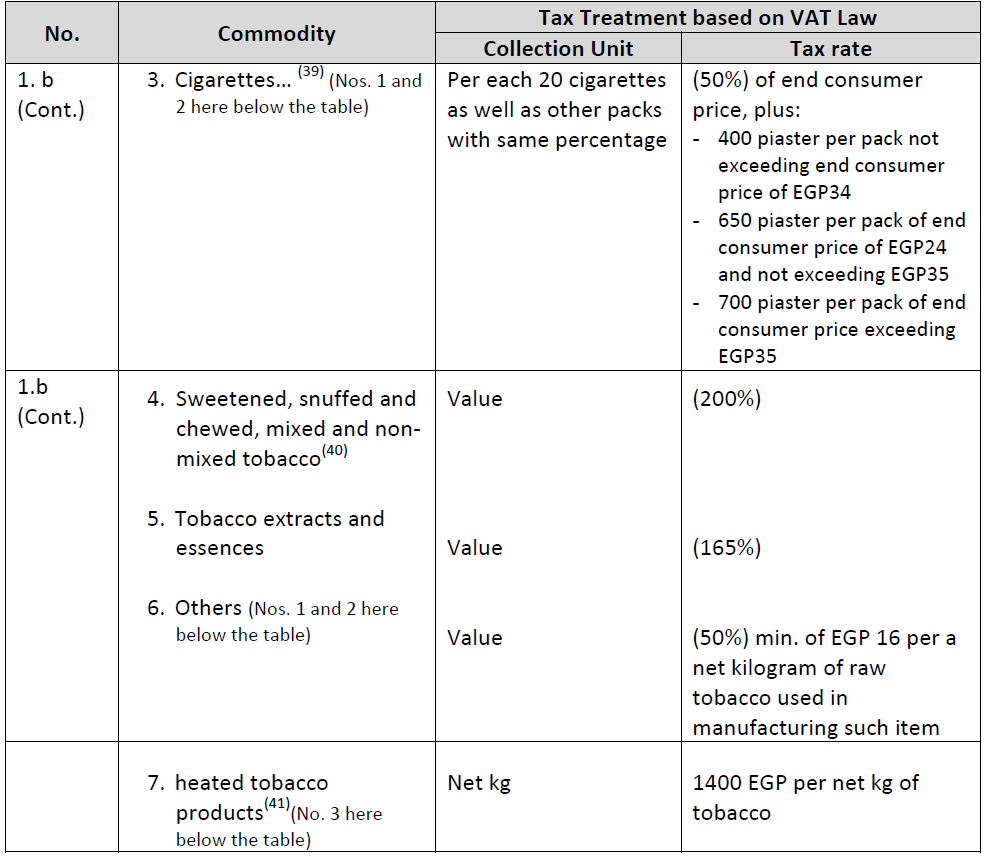

1) Prices of product sold to end consumer and declared on the date of enforcement of this law shall be the minimum tax base for calculating Table Tax due on such items.

2) Table Tax shall be collected on total end consumer price (inclusive of all taxes and dues) from producers or importers upon custom clearance.

3) This items includes manufactured tobacco which use thereof generates vapor without combustion of tobacco. Tobacco may take the form of tobacco sticks ,capsules or any other form.

4) This item includes any liquid consumed by e- cigarettes whether including nicotine or not.

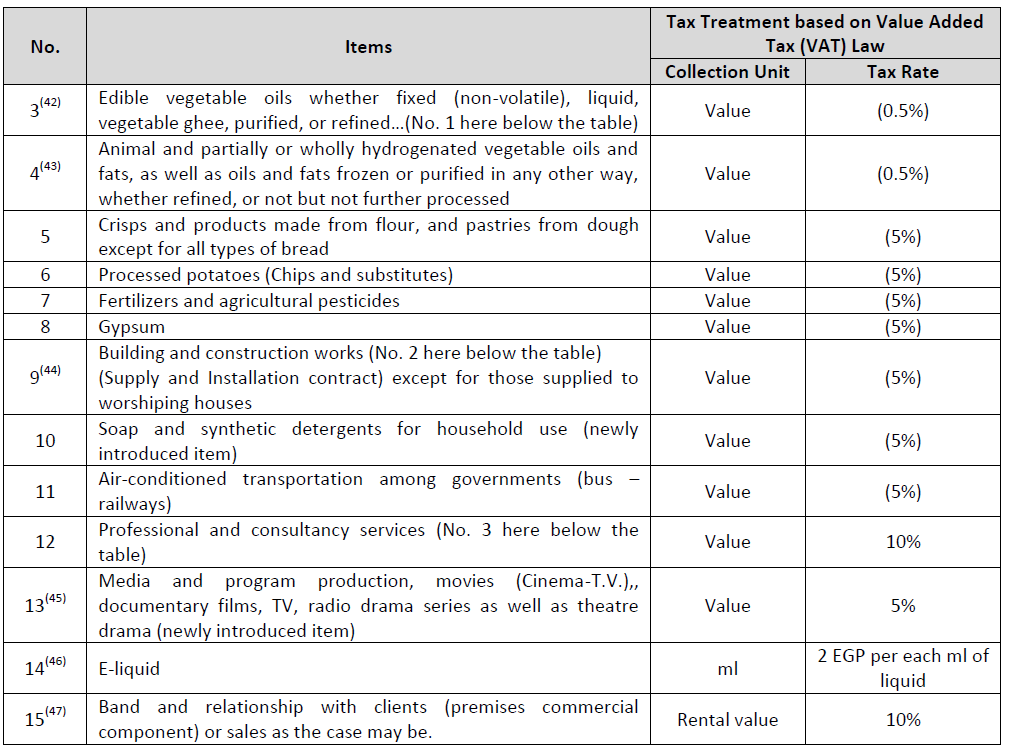

1) Importer and producer shall notify ETA of a list of entities which purchased such items, and/or of the manner of disposal of the sold quantities of such items within fifteen (15) days following the month of sale.

2) Value means the value of the extract approved by the consultant, and the table tax previously paid by the subcontractor is settled from the table tax paid by the main contractor for the same works.

3) value means actual value paid in consideration of service and this item does not include services provided by craftsmen.

1) Value shall mean the selling price for end consumer.

2) VAT and Table Tax shall be collected from producer and/or importer upon customs clearance on total price for end consumer.