Cases

[NB: The definition of 'enterprise' has been amended by s. 23 (1) (e) of the Taxation Laws Amendment Act 27 of 1997, a provision which will be put into operation by proclamation. See PENDLEX. A definition of 'customs secured area' has been inserted by s. 148 (1) of the Second Revenue Laws Amendment Act 60 of 2001, a provision which will be put into operation by proclamation.]

In this Act, unless the context otherwise indicates-

'adjusted cost' means the cost of any goods or services where tax has been charged or would have been charged if section 7 of this Act had been applicable prior to the commencement date, in respect of the supply of goods and services or if the vendor was or would have been entitled to an input tax deduction in terms of paragraph (b) of the definition of 'input

tax';

[Definition of 'adjusted cost' inserted by s. 164 (1) (a) of Act 45 of 2003.]

'ancillary transport services' means stevedoring services, lashing and securing services, cargo inspection services, preparation of customs documentation, container handling services and storage of transported goods or goods to be transported;

'association not for gain' means-

(a) any religious institution of a public character; or

(b) any other society, association or organization, whether incorporated or not (other than an educational institution in respect of which the provisions of paragraph (c) apply), which-

(i) is carried on otherwise than for the purposes of profit or gain to any proprietor, member or shareholder; and

(ii) is, in terms of its memorandum, articles of association, written rules or other document constituting or governing the activities of that society, association or organisation-

(aa) required to utilize any property or income solely in the furtherance of its aims and objects; and

(bb) prohibited from transferring any portion thereof directly or indirectly in any manner whatsoever so as to profit any person other than by way of the payment in good faith of

reasonable remuneration to any officer or employee of the society, association or organization for any services actually rendered to such society, association or organization; and

(cc) upon the winding-up or liquidation of such society, association or organization, obliged to give or transfer its assets remaining after the satisfaction of its liabilities to some other society, association or organization with objects similar to those of the said society, association or organization; or

[Para. (b) substituted by s. 23 (1) (a) of Act 27 of 1997.]

(c) any educational institution of a public character, whether incorporated or not, which-

(i) is carried on otherwise than for the purposes of profit or gain to any proprietor, member or

shareholder; and

(ii) is, in terms of its memorandum, articles of association, written rules or other document constituting or governing the activities of that educational institution-

(aa) required to utilize any property or income solely in the furtherance of its aims and objects; and

(bb) prohibited from transferring any portion thereof directly or indirectly in any manner whatsoever so as to profit any person other than by way of the payment in good faith of reasonable remuneration to any officer or employee of the educational institution for any services actually rendered to such institution;

[Para. (c) added by s. 23 (1) (b) of Act 27 of 1997.]

'business day' means any day which is not a Saturday, Sunday or public holiday;

'cash value', in relation to the supply of goods supplied under an instalment credit agreement, means-

(a) where the seller or lessor is a banker or financier, an amount equal to or exceeding the sum of the cost to the banker or financier of the goods, including any cost of erection, construction, assembly or installation of the goods borne by the banker or financier and the tax leviable under section 7 (1) (a) in respect of such supply by the banker or financier; or

(b) where the seller or lessor is a dealer, an amount equal to or exceeding the price (including tax) at which the goods are normally sold by him for cash or may normally be acquired from him for cash (including tax) and any charge (including tax) made by the seller or lessor in respect of the erection, construction, assembly or installation of the goods if such charge is financed by the seller or lessor under the instalment credit agreement;

'Chief Executive Officer' ......

[Definition of 'Chief Executive Officer' inserted by s. 18 (a) of Act 37 of 1996 and deleted by s. 34 (1) of Act 34 of 1997.]

'close corporation' means a close corporation within the meaning of the Close Corporations Act, 1984 (Act 69 of 1984);

'commencement date' means 30 September 1991;

[Definition of 'commencement date' substituted by s. 21 (a) of Act 136 of 1991.]

'commercial accommodation' means-

(a) lodging or board and lodging, together with domestic goods and services, in any house, flat, apartment, room, motel, hotel, inn, guest house, boarding house, residential establishment, holiday accommodation unit, chalet, tent, caravan, camping site, houseboat or similar establishment, which is regularly or systematically supplied and where the total annual receipts from the supply thereof exceeds R60 000 per annum or is reasonably expected to exceed R60 000 per annum, but excluding a dwelling supplied in terms of an agreement for the letting and hiring thereof;

[Para. (a) substituted by s. 47 of Act 12 of 2003.]

(b) lodging or board and lodging in a home for the aged, children, physically or mentally handicapped persons; and

(c) lodging or board and lodging in a hospice;

[Definition of 'commercial accommodation' inserted by s. 65 (1) (a) of Act 19 of 2001 and substituted by s. 148 (1) (a) of Act 60 of 2001.]

'commercial rental establishment' ......

[Definition of 'commercial rental establishment' substituted by s. 12 (1) (a) of Act 136 of 1992, amended by s. 81 (1) of Act 53 of 1999 and deleted by s. 65 (1) (b) of Act 19 of 2001.]

'Commissioner' means the Commissioner for the South African Revenue Service;

[Definition of 'Commissioner' substituted by s. 34 (1) of Act 34 of 1997.]

'company' means a company as defined in section 1 of the Income Tax Act;

'connected persons' means-

(a) any natural person (including the estate of a natural person if such person is deceased or insolvent) and-

(i) any relative of that natural person (being a relative as defined in section 1 of the Income Tax Act) or the estate of any such relative if the relative is deceased or insolvent; or

(ii) any trust fund in respect of which any such relative or such estate of such relative is or may be a beneficiary; or

[Para. (a) substituted by s. 22 (a) of Act 97 of 1993.]

(b) any trust fund and any person who is or may be a beneficiary in respect of that fund; or

(c) any partnership or close corporation and-

(i) any member thereof; or

(ii) any other person where that person and a member of such partnership or close corporation, as the case may be, are connected persons in terms of this definition; or

(d) any company (other than a close corporation) and-

(i) any person (other than a company) where that person, his spouse or minor child or any trust fund in respect of which that person, his spouse or minor child is or may be a beneficiary, is separately interested or two or more of them are in the aggregate interested in 10 per cent or more of the company's paid-up capital or 10 per cent or more of the company's equity share capital (as defined in section 1 of the Income Tax Act) or 10 per cent or more of the voting rights of the shareholders of the company, whether directly or indirectly; or

(ii) any other company the shareholders in which (being shareholders as contemplated in the

definition of 'shareholder' in section 1 of the Income Tax Act) are substantially the same persons

as the shareholders in the first-mentioned company, or which is controlled by the same persons who control the first-mentioned company; or

(iii) any person where that person and the person referred to in subparagraph (i) or his spouse or minor child or the trust fund referred to in that subparagraph or the other company referred to in

subparagraph (ii) are connected persons in terms of this definition; or

(e) any separate enterprise, branch or division of a vendor which is separately registered as a vendor under the provisions of section 50 and any other such enterprise, branch or division of the vendor; or

(f) any branch, division or separate enterprise of an association not for gain which is deemed by subsection

(5) of section 23 to be a separate person for the purposes of that section and any other branch, division or separate enterprise of that association, whether or not such other branch, division or separate enterprise is a vendor; or

(g) any person and any superannuation scheme referred to in section 2 (2) (vii), the members of which are mainly the employees or office holders or former employees or office holders of that person;

[Para. (g) added by s. 23 (1) (d) of Act 27 of 1997.]

'consideration', in relation to the supply of goods or services to any person, includes any payment made or to be made (including any deposit on any returnable container and tax), whether in money or otherwise, or any act or forbearance, whether or not voluntary, in respect of, in response to, or for the inducement of, the supply of any goods or services, whether by that person or by any other person, but does not include any payment made by any person as a donation to any association not for gain: Provided that a deposit (other than a deposit on a returnable container), whether refundable or not, given in respect of a supply of goods or services shall not be considered as payment made for the supply unless and until the supplier applies the deposit as consideration for the supply or such deposit is forfeited;

[Definition of 'consideration' substituted by s. 92 (1) (a) of Act 32 of 2004 and amended by s. 8 (1) of Act 10 of 2005.]

'consideration in money' includes consideration expressed as an amount of money;

'Controller' has the meaning assigned thereto in section 1 of the Customs and Excise Act;

[Definition of 'Controller' inserted by s. 101 (a) of Act 31 of 2005.]

'Customs and Excise Act' means the Customs and Excise Act, 1964 (Act 91 of 1964);

'customs controlled area' has the meaning assigned thereto in section 21A of the Customs and Excise Act;

[Definition of 'customs controlled area' inserted by s. 164 (1) (c) of Act 45 of 2003.]

'customs controlled area enterprise' has the meaning assigned thereto in section 21A of the Customs and Excise Act, 1964;

[Definition of 'customs controlled area enterprise' inserted by s. 164 (1) (c) of Act 45 of 2003.]

'designated entity' means a vendor-

(i) to the extent that its supplies of goods and services of an activity carried on by that vendor are in terms of

(b) (i) of the definition of 'enterprise' treated as supplies made in the course or furtherance of an

enterprise;

(ii) which is a major public entity, national government business enterprise or provincial government business enterprise listed in Schedule 2 or Part B or D of Schedule 3 of the Public Finance Management Act, 1999 (Act 1 of 1999), respectively; or

(iii) which is a 'Public Private Partnership' as defined in Regulation 16 of the Treasury Regulations issued in terms of section 76 of the Public Finance Management Act, 1999 (Act 1 of 1999): or

(iv) which is a welfare organisation;

[Definition of 'designated entity' inserted by s. 164 (1) (c) of Act 45 of 2003.]

'domestic goods and services' means goods and services provided in any enterprise supplying commercial accommodation, including-

(a) cleaning and maintenance;

(b) electricity, gas, air conditioning or heating;

(c) a telephone, television set, radio or other similar article;

(d) furniture and other fittings;

(e) meals;

(f) laundry; or

[Para. (f) added by s. 92 (1) (c) of Act 32 of 2004.]

(g) nursing services;

[Para. (g) added by s. 92 (1) (c) of Act 32 of 2004.]

[Definition of 'domestic goods and services' substituted by s. 65 (1) (c) of Act 19 of 2001 and by s. 148 (1) (c) of Act 60 of 2001.]

'donated goods or services' means goods or services which are donated to an association not for gain and are intended for use in the carrying on or carrying out of the purposes of that association;

'donation' means a payment whether in money or otherwise voluntarily made to any association not for gain for the carrying on or the carrying out of the purposes of that association and in respect of which no identifiable direct valuable benefit arises or may arise in the form of a supply of goods or services to the person making that payment or in the form of a supply of goods or services to any other person who is a connected person in relation to the person making the payment, but does not include any payment made by a public authority or a local authority;

[Definition of 'donation' inserted s. 92 (1) (d) of Act 32 of 2004.]

'dwelling' means, except where it is used in the supply of commercial accommodation, any building, premises, structure, or any other place, or any part thereof, used predominantly as a place of residence or abode of any natural person or which is intended for use predominantly as a place of residence or abode of any natural person, including fixtures and fittings belonging thereto and enjoyed therewith;

[Definition of 'dwelling' substituted by s. 12 (1) (b) of Act 136 of 1992, by s. 65 (1) (d) of Act 19 of 2001 and by s. 148 (1) (d) of Act 60 of 2001.]

'employee organization' means an organization in which a number of employees in any particular undertaking, industry, trade, occupation or profession are associated together for the purpose of regulating relations between themselves or some of them and their employers or some of their employers or mainly for that purpose, disregarding the provision of sickness, accident or unemployment benefits for the members of the organization or for the widows, children, dependants or nominees of deceased members;

[Definition of 'employee organization' inserted by Government Notice 2695 of 8 November 1991 and by s. 12 (1) (c) of Act

136 of 1992.]

'enterprise' means-

(a) in the case of any vendor other than a local authority, any enterprise or activity which is carried on continuously or regularly by any person in the Republic or partly in the Republic and in the course or furtherance of which goods or services are supplied to any other person for a consideration, whether or not for profit, including any enterprise or activity carried on in the form of a commercial, financial, industrial, mining, farming, fishing or professional concern or any other concern of a continuing nature or in the form of an association or club;

(b) without limiting the applicability of paragraph (a) in respect of any activity carried on in the form of a commercial, financial, industrial, mining, farming, fishing or professional concern-

(i) the making of supplies by any public authority of goods or services which the Minister, having

regard to the circumstances of the case, is satisfied are of the same kind or are similar to taxable

supplies of goods or services which are or might be made by any person other than such public

authority in the course or furtherance of any enterprise, if the Commissioner, in pursuance of a

decision of the Minister under this subparagraph, has notified such public authority that its supplies of such goods or services are to be treated as supplies made in the course or furtherance of an enterprise;

(ii) the activities of any welfare organization as respects activities referred to in the definition of 'welfare organization' in this section;

(iii) the activities of any share block company (other than the services in respect of which section 12 (f) applies) where such company has applied for registration as a vendor under the provisions of

section 23 (3) and has been registered as such;

[Sub-para. (iii) added by s. 12 (1) (d) of Act 136 of 1992.]

[NB: A sub-para. (iv) has been inserted by s. 23 (1) (e) of the Taxation Laws Amendment Act 27 of 1997, a provision which will be put into operation by proclamation. See PENDLEX.]

(v) the activities of a foreign donor funded project;

[Sub-para. (v) added by s. 101 (b) of Act 31 of 2005.]

(c) in the case of a vendor which is a local authority, any activity in the course or furtherance of which any of the following supplies of goods or services are made:

(i) The supply of electricity, gas or water;

(ii) the supply of services consisting of the drainage, removal or disposal of sewage or garbage;

(iii) the supply of goods or services incidental to or necessary for the supply of goods or services in

respect of which the provisions of subparagraph (i) or (ii) apply;

(iv) the making of supplies of goods or services in the course of any business carried on by such local authority, if-

(aa) such supplies are of the same kind or are similar to taxable supplies of goods or services which are or might be made by any person other than such local authority in the course or furtherance of any enterprise; and

(bb) the revenue normally derived by such local authority for its own benefit from making such

supplies, together with any grant or subsidy paid to that local authority by the State or any person for the purposes of such business, is, or may reasonably be expected to be, sufficient to fund the expenditure (excluding expenditure of a capital nature but including a reasonable provision for depreciation in the value of the assets of the business by reason of wear and tear and obsolescence) incurred by that local authority in the production of such revenue; and

(cc) (A) such business falls within a category of businesses which the Minister, having regard to the provisions of items (aa) and (bb) as generally applicable, has by notice in the Gazette determined to be a category of businesses in respect of which the provisions of this subparagraph shall be deemed to apply; or (B) such business (not being a business falling within a category referred to in subitem (A)) is determined by the Minister, having regard to the provisions of items (aa) and (bb) as applicable in the case of such business, to be a business in respect of which the provisions of this subparagraph shall be deemed to apply and the Commissioner, in pursuance of the Minister's determination under this subitem, has notified such local authority accordingly, and, in the case of a regional services council, a joint services board or a transitional metropolitan council, any other activities of that council or board to the extent that they are financed by levies referred to in section 8 (6) (b):

[Sub-para. (iv) amended by s. 9 (1) (a) of Act 20 of 1994.]

[Para. (c) amended by s. 22 (b) of Act 97 of 1993.]

Provided that-

(i) anything done in connection with the commencement or termination of any such enterprise or activity shall be deemed to be done in the course or furtherance of that enterprise or activity;

(ii) any branch or main business of an enterprise permanently situated at premises outside the Republic shall be deemed to be carried on by a person separate from the vendor, if-

(aa) the branch or main business can be separately identified; and(b) without limiting the applicability of paragraph (a) in respect of any activity carried on in the form

of a commercial, financial, industrial, mining, farming, fishing or professional concern-

(i) the making of supplies by any public authority of goods or services which the Minister, having

regard to the circumstances of the case, is satisfied are of the same kind or are similar to taxable

supplies of goods or services which are or might be made by any person other than such public

authority in the course or furtherance of any enterprise, if the Commissioner, in pursuance of a

decision of the Minister under this subparagraph, has notified such public authority that its

supplies of such goods or services are to be treated as supplies made in the course or furtherance

of an enterprise;

(ii) the activities of any welfare organization as respects activities referred to in the definition of

'welfare organization' in this section;

(iii) the activities of any share block company (other than the services in respect of which section 12 (f) applies) where such company has applied for registration as a vendor under the provisions of

section 23 (3) and has been registered as such;

[Sub-para. (iii) added by s. 12 (1) (d) of Act 136 of 1992.]

[NB: A sub-para. (iv) has been inserted by s. 23 (1) (e) of the Taxation Laws Amendment Act 27 of 1997, a provision which will be put into operation by proclamation. See PENDLEX.]

(v) the activities of a foreign donor funded project;

[Sub-para. (v) added by s. 101 (b) of Act 31 of 2005.]

(c) in the case of a vendor which is a local authority, any activity in the course or furtherance of which any of the following supplies of goods or services are made:

(i) The supply of electricity, gas or water;

(ii) the supply of services consisting of the drainage, removal or disposal of sewage or garbage;

(iii) the supply of goods or services incidental to or necessary for the supply of goods or services in

respect of which the provisions of subparagraph (i) or (ii) apply;

(iv) the making of supplies of goods or services in the course of any business carried on by such local authority, if-

(aa) such supplies are of the same kind or are similar to taxable supplies of goods or services which are or might be made by any person other than such local authority in the course or furtherance of any enterprise; and

(bb) the revenue normally derived by such local authority for its own benefit from making such

supplies, together with any grant or subsidy paid to that local authority by the State or any person for the purposes of such business, is, or may reasonably be expected to be, sufficient to fund the expenditure (excluding expenditure of a capital nature but including a reasonable provision for depreciation in the value of the assets of the business by reason of wear and tear and obsolescence) incurred by that local authority in the production of such revenue; and

(cc) (A) such business falls within a category of businesses which the Minister, having regard to the provisions of items (aa) and (bb) as generally applicable, has by notice in the Gazette determined to be a category of businesses in respect of which the provisions of this subparagraph shall be deemed to apply; or

(B) such business (not being a business falling within a category referred to in subitem

(A)) is determined by the Minister, having regard to the provisions of items (aa) and (bb) as applicable in the case of such business, to be a business in respect of which the provisions of this subparagraph shall be deemed to apply and the Commissioner, in pursuance of the Minister's determination under this subitem, has notified such local authority accordingly, and, in the case of a regional services council, a joint services board or a transitional metropolitan council, any other activities of that council or board to the extent that they are financed by levies referred to in section 8 (6) (b):

[Sub-para. (iv) amended by s. 9 (1) (a) of Act 20 of 1994.]

[Para. (c) amended by s. 22 (b) of Act 97 of 1993.]

Provided that-

(i) anything done in connection with the commencement or termination of any such enterprise or activity shall be deemed to be done in the course or furtherance of that enterprise or activity;

(ii) any branch or main business of an enterprise permanently situated at premises outside the Republic shall be deemed to be carried on by a person separate from the vendor, if-

(aa) the branch or main business can be separately identified; and

(bb) an independent system of accounting is maintained by the concern in respect of the branch or main business;

[Para. (ii) substituted by s. 22 (c) of Act 97 of 1993, by s. 9 (1) (b) of Act 20 of 1994 and by s. 92 (1) (e) of Act 32 of 2004.]

(iii) (aa) the rendering of services by an employee to his employer in the course of his employment or the rendering of services by the holder of any office in performing the duties of his office, shall not be deemed to be the carrying on of an enterprise to the extent that any amount constituting

remuneration as contemplated in the definition of remuneration' in paragraph 1 of the Fourth

Schedule to the Income Tax Act is paid or is payable to such employee or office holder, as the case

may be;

[Item (aa) substituted by s. 164 (1) (f) of Act 45 of 2003.]

(bb) subparagraph (aa) of this paragraph shall not apply in relation to any employment or office

accepted by any person in carrying on any enterprise carried on by him independently of the employer or concern by whom the amount of remuneration is paid or payable;

(iv) any activity carried on by a natural person essentially as a private or recreational pursuit or hobby or any activity carried on by a person other than a natural person which would, if it were carried on by a natural person, be carried on essentially as a private or recreational pursuit or hobby shall not be deemed to be the carrying on of an enterprise;

(v) any activity shall to the extent to which it involves the making of exempt supplies not be deemed to be the carrying on of an enterprise;

(vi) the activity of underwriting insurance business by Underwriting Members of Lloyd's of London, to the extent that contracts of insurance are concluded in the Republic, shall be deemed to be the carrying on of an enterprise;

[Para. (vi) added by Government Notice 2695 of 8 November 1991 and by s. 12 (1) (e) of Act 136 of 1992 and substituted by s. 81 (1) (e) of Act 53 of 1999.]

(vii) the activities of the Road Accident Fund contemplated in the Road Accident Fund Act, 1996 (Act 56 of 1996), shall be deemed not to be the carrying on of an enterprise;

[Para. (vii) added by s. 9 (1) (c) of Act 20 of 1994 and substituted by s. 114 (1) (a) of Act 74 of 2002.]

(viii) the making of supplies by a constitutional institution listed in Schedule 1 of the Public Finance

Management Act, 1999 (Act 1 of 1999), shall be deemed not to be the carrying on of an enterprise;

[Para. (viii) inserted by s. 164 (1) (g) of Act 45 of 2003.]

(ix) where a person carries on or intends carrying on an enterprise or activity supplying commercial

accommodation as contemplated in paragraph (a) of the definition of 'commercial accommodation' in section 1, and the total value of taxable supplies made by that person in the preceding period of 12 months or which it can reasonably be expected that that person will make in a period of 12 months, as the case may be, will not exceed R60 000, shall be deemed not to be the carrying on of an enterprise;

[Para. (ix) added by s. 92 (1) (f) of Act 32 of 2004.]

[Definition of 'enterprise' amended by s. 21 (b) of Act 136 of 1991.]

'entertainment' means the provision of any food, beverages, accommodation, entertainment, amusement, recreation or hospitality of any kind by a vendor whether directly or indirectly to anyone in connection with an enterprise carried on by him;

'exempt supply' means a supply that is exempt from tax under section 12;

'export country' means any country other than the Republic and includes any place which is not situated in the Republic: Provided that the President may by notice in the Gazette determine that a specific country or territory shall from a date and to the extent indicated in the notice, be deemed not to be an export country;

[Definition of 'export country' substituted by s. 12 (1) (f) of Act 136 of 1992 and by s. 9 (1) (d) of Act 20 of 1994.]

'exported' , in relation to any movable goods supplied by any vendor under a sale or an instalment credit agreement, means-

(a) consigned or delivered by the vendor to the recipient at an address in an export country as evidenced by documentary proof acceptable to the Commissioner; or

(b) delivered by the vendor to the owner or charterer of any foreign-going ship contemplated in paragraph (a) of the definition of 'foreign-going ship' or to a foreign-going aircraft when such ship or aircraft is going to a destination in an export country and such goods are for use or consumption in such ship or aircraft, as the case may be; or

(c) delivered by the vendor to the owner or charterer of any foreign-going ship contemplated in paragraph (b) of the definition of 'foreign-going ship' for use in such ship; or

(d) removed from the Republic by the recipient for conveyance to an export country in accordance with the provisions of an export incentive scheme approved by the Minister;

[Para. (d) amended by s. 22 (d) of Act 97 of 1993 and substituted by s. 9 (1) (e) of Act 20 of 1994.]

'financial services' means the activities which are deemed by section 2 to be financial services;

'fixed property' means land (together with improvements affixed thereto), any unit as defined in section 1 of the Sectional Titles Act, 1986 (Act 95 of 1986), any share in a share block company which confers a right to or an interest in the use of immovable property, and, in relation to a property time -sharing scheme, any time -sharing interest as defined in section 1 of the Property Time-sharing Control Act, 1983 (Act 75 of 1983), and any real right in any such land, unit, share or time -sharing interest;

[Definition of 'fixed property' substituted by Government Notice 2695 of 8 November 1991 and by s. 12 (1) (g) of Act 136 of 1992.]

'foreign donor funded project' means a project established as a result of an international donor funding agreement to which the Government of the Republic is a party, to supply goods or services to beneficiaries;

[Definition of 'foreign donor funded project' inserted by s. 101 (c) of Act 31 of 2005.]

'foreign-going aircraft' means any aircraft engaged in the transportation for reward of passengers or goods wholly or mainly on flights between airports in the Republic and airports in export countries or between airports in export countries;

[Definition of 'foreign-going aircraft' substituted by s. 9 (1) (f) of Act 20 of 1994.]

'foreign-going ship' means-

(a) any ship or other vessel engaged in the transportation for reward of passengers or goods wholly or mainly on voyages between ports in the Republic and ports in export countries or between ports in export countries; or

(b) any ship or other vessel registered in an export country where such ship or vessel is utilized for the purposes of a commercial, fishing or other concern conducted outside the Republic by a person who is not a vendor and is not a resident of the Republic;

[Definition of 'foreign-going ship' substituted by s. 9 (1) (g) of Act 20 of 1994.]

'goods' means corporeal movable things, fixed property and any real right in any such thing or fixed property, but excluding-

(a) money;

(b) any right under a mortgage bond or pledge of any such thing or fixed property; and

(c) any stamp, form or card which has a money value and has been sold or issued by the State for the payment of any tax or duty levied under any Act of Parliament, except when subsequent to its original sale or issue it is disposed of or imported as a collector's piece or investment article;

'grant' means any appropriation, grant in aid, subsidy or contribution transferred, granted or paid to a vendor by a public authority, local authority or constitutional institution listed in Schedule 1 to the Public Finance Management Act, 1999 (Act 1 of 1999), but does not include-

(a) a payment made for the supply of any goods or services to that public authority or local authority, including all goods or services supplied to a public authority, local authority or constitutional institution listed in Schedule 1 to the Public Finance Management Act, 1999 (Act 1 of 1999) in accordance with a procurement process prescribed-

(i) in terms of the Regulations issued under section 76 (4) (c) of the Public Finance Management Act, 1999 (Act 1 of 1999); or

(ii) in terms of Chapter 11 of the Local Government: Municipal Finance Management Act, 2003 (Act 56 of 2003), or any other similar process; or

(b) a payment contemplated in section 8 (23);

[Definition of 'grant' inserted by s. 92 (1) (g) of Act 32 of 2004.]

'imported services' means a supply of services that is made by a supplier who is resident or carries on business outside the Republic to a recipient who is a resident of the Republic to the extent that such services are utilized or consumed in the Republic otherwise than for the purpose of making taxable supplies;

'Income Tax Act' means the Income Tax Act, 1962 (Act 58 of 1962);

'Industrial Development Zone (IDZ)' has the meaning assigned thereto in section 21A of the Customs and Excise Act;

[Definition of 'Industrial Development Zone' inserted by s. 148 (1) (e) of Act 60 of 2001 and substituted by s. 164 (1) (i) of Act 45 of 2003.]

'Industrial Development Zone (IDZ) operator' has the meaning assigned thereto in terms of section 21A of the Customs and Excise Act;

[Definition of 'Industrial Development Zone (IDZ) operator' inserted by s. 164 (1) (j) of Act 45 of 2003.]

'input tax', in relation to a vendor, means-

(a) tax charged under section 7 and payable in terms of that section by-

(i) a supplier on the supply of goods or services made by that supplier to the vendor; or

(ii) the vendor on the importation of goods by him; or

(iii) the vendor under the provisions of section 7 (3);

(b) an amount equal to the tax fraction (being the tax fraction applicable at the time the supply is deemed to have taken place) of the lesser of any consideration in money given by the vendor for or the open market value of the supply (not being a taxable supply) to him by way of a sale on or after the commencement date by a resident of the Republic of any second-hand goods situated in the Republic: Provided that where such second-hand goods consist of-

(i) fixed property in respect of the acquisition of which transfer duty is, in terms of the Transfer Duty Act, payable or would have been payable had an exemption from transfer duty (whether in terms of the Transfer Duty Act or any other Act of Parliament) not been applicable; or

(ii) a share in a share block company in respect of the original issue or registration of transfer of which stamp duty is, in terms of the Stamp Duties Act, payable or would have been payable had an

exemption from stamp duty (whether in terms of the Stamp Duties Act or any other Act of Parliament) not been applicable,

[Para. (b) amended by s. 23 (1) (f) of Act 27 of 1997.]

such amount shall not exceed the amount of transfer duty or stamp duty, as the case may be, which is or would have been payable in respect of such acquisition, original issue or registration of transfer, as the case may be; and

[Para. (b) substituted by Government Notice 2695 of 8 November 1991 and by s. 12 (1) (h) of Act 136 of 1992, amended by s. 22 (e) of Act 97 of 1993 and substituted by s. 9 (1) (h) of Act 20 of 1994.]

(c) an amount equal to the tax fraction of the consideration in money deemed by section 10 (16) to be for the supply (not being a taxable supply) by a debtor to the vendor of goods repossessed under an instalment credit agreement: Provided that the tax fraction applicable under this paragraph shall be the tax fraction applicable at the time of supply of the goods to the debtor under such agreement as contemplated in section 9 (3) (c), where the goods or services concerned are acquired by the vendor wholly for the purpose of consumption, use or supply in the course of making taxable supplies or, where the goods or services are acquired by the vendor partly for such purpose, to the extent (as determined in accordance with the provisions of section 17) that the goods or services concerned are acquired by the vendor for such purpose;

'instalment credit agreement' means any agreement entered into on or after the commencement date whereby any goods consisting of corporeal movable goods or of any machinery or plant, whether movable or immovable-

(a) are supplied under a sale under which-

(i) the goods are sold by the seller to the purchaser against payment by the purchaser to the seller of a stated or determinable sum of money at a stated or determinable future date or in whole or in part in instalments over a period in the future; and

(ii) such sum of money includes finance charges stipulated in the agreement of sale; and

(iii) the aggregate of the amounts payable by the purchaser to the seller under such agreement exceeds the cash value of the supply; and

(iv) (aa) the purchaser does not become the owner of those goods merely by virtue of the delivery to or the use, possession or enjoyment by him thereof; or

(bb) the seller is entitled to the return of those goods if the purchaser fails to comply with any term of that agreement; or

(b) are supplied under a lease under which-

(i) the rent consists of a stated or determinable sum of money payable at a stated or determinable

future date or periodically in whole or in part in instalments over a period in the future; and

(ii) such sum of money includes finance charges stipulated in the lease; and

(iii) the aggregate of the amounts payable under such lease by the lessee to the lessor for the period of such lease (disregarding the right of any party thereto to terminate the lease before the end of such period) and any residual value of the leased goods on termination of the lease, as stipulated in the lease, exceeds the cash value of the supply; and

(iv) the lessee is entitled to the possession, use or enjoyment of those goods for a period of at least 12 months; and

(v) the lessee accepts the full risk of destruction or loss of, or other disadvantage to, those goods and assumes all obligations of whatever nature arising in connection with the insurance, maintenance and repair of those goods while the agreement remains in force;

'insurance' means insurance or guarantee against loss, damage, injury or risk of any kind whatever, whether pursuant to any contract or law, and includes reinsurance; and 'contract of insurance' includes a policy of insurance, an insurance cover, and a renewal of a contract of insurance: Provided that nothing in this definition shall apply to any insurance specified in section 2;

'invoice' means a document notifying an obligation to make payment;

'licensed customs and excise storage warehouse' means a warehouse licensed by the Commissioner at any place appointed for that purpose under the provisions of the Customs and Excise Act, which has been approved by the Commissioner for the storage of goods as he may approve in respect of that warehouse;

[Definition of 'licensed customs and excise storage warehouse' inserted by s. 101 (d) of Act 31 of 2005.]

'local authority' means-

(a) any divisional council, rural council, municipal council, regional services council, town board, local board, village management board or health committee or any joint services board established under the KwaZulu and Natal Joint Services Act, 1990 (Act 84 of 1990);

(b) any other body, council, board, committee or institution established or deemed to be established by or under any law which has functions similar to those of the councils, boards and committees enumerated in paragraph (a) and which may levy rates on the value of immovable property within its area of jurisdiction or receive payments for services rendered or to be rendered; and

(c) any water board or regional water services corporation or any other institution which has powers similar to those of any such boards or corporations:

Provided that where any local authority has been disestablished and superseded by a new local authority in terms of the Local Government: Municipal Structures Act, 1998 (Act 117 of 1998), such disestablished local authority and such new local authority shall for the purposes of this Act be deemed to be and to have been one and the same local authority;

[Definition of 'local authority' amended by s. 64 (a) of Act 59 of 2000.]

'Minister' means the Minister of Finance;

'money' means-

(a) coins (other than coins made wholly or mainly from a precious metal other than silver) which the South African Reserve Bank has issued in the Republic in accordance with the provisions of section 14 of the South African Reserve Bank Act, 1989 (Act 90 of 1989), or which remain in circulation as contemplated in the proviso to subsection (1) of that section, and any paper currency which under the said Act is a legal tender;

(b) (i) any coin (other than a coin made wholly or mainly from a precious metal) or paper currency of any country other than the Republic which is used or circulated or is intended for use or circulation as currency;

(ii) any bill of exchange, promissory note, bank draft, postal order or money order, except when disposed of or imported as a collector's piece, investment article or item of numismatic interest;

'month' means any of the twelve portions into which any calendar year is divided;

[Definition of 'month' inserted by s. 164 (1) (k) of Act 45 of 2003.]

'motor car' includes a motor car, station wagon, minibus, double cab light delivery vehicle and any other motor vehicle of a kind normally used on public roads, which has three or more wheels and is constructed or converted wholly or mainly for the carriage of passengers, but does not include-

(a) vehicles capable of accommodating only one person or suitable for carrying more than 16 persons; or

(b) vehicles of an unladen mass of 3 500 kilograms or more; or

(c) caravans and ambulances;

(d) vehicles constructed for a special purpose other than the carriage of persons and having no

accommodation for carrying persons other than such as is incidental to that purpose;

(e) game viewing vehicles (other than sedans, station wagons, minibuses or double cab light delivery vehicles) constructed or permanently converted for the carriage of seven or more passengers for game viewing in national parks, game reserves, sanctuaries or safari areas and used exclusively for that purpose, other than use which is merely incidental and subordinate to that use; or [Para. (e) added by s. 92 (1) (j) of Act 32 of 2004.]

(f) vehicles, constructed as or permanently converted into hearses for the transport of deceased persons and used exclusively for that purpose;

[Para. (f) added by s. 92 (1) (j) of Act 32 of 2004.]

[Definition of 'motor car' amended by s. 76 of Act 30 of 2000 and by s. 92 (1) (h) of Act 32 of 2004.]

'open market value' in relation to the supply of goods or services, means the open market value thereof determined in accordance with the provisions of section 3;

'output tax', in relation to any vendor, means the tax charged under section 7 (1) (a) in respect of the supply of goods and services by that vendor;

'person' includes any public authority, any local authority, any company, any body of persons (corporate or unincorporate), the estate of any deceased or insolvent person, any trust fund and any foreign donor funded project;

[Definition of 'person' substituted by s. 101 (e) of Act 31 of 2005.]

'precious metals' means gold, silver, platinum, iridium and any other metals of the platinum group, and any other metal which the State President has by proclamation in the Gazette declared to be a precious metal for the purpose of this Act;

'prescribed rate' in relation to any interest payable in terms of this Act means a rate equal to the rate fixed from time to time by the Minister by notice in the Gazette in terms of section 80 (1) (b) of the Public Finance Management Act, 1999 (Act 1 of 1999): Provided that where the Minister fixes a new rate in terms of that Act, that new rate applies for purposes of this Act from the first day of the second month following the date on which that new rate came into operation;

[Definition of 'prescribed rate' inserted by s. 1 of Act 61 of 1993, amended by s. 9 of Act 20 of 1994, by GN 1505 of 20 November 1998, by GN 541 of 22 April 1999, by GN 1065 of 1 September 1999, by GN 184 of 25 February 2000 and by GN 1160 of 13 September 2002 and substituted by s. 114 (1) (b) of Act 74 of 2002 and by s. 43 (a) of Act 16 of 2004.]

'prescribed tax rate' ......

[Definition of 'prescribed tax rate' deleted by s. 21 (c) of Act 136 of 1991.]

'public authority' means-

(i) any department or division of the public service as listed in Schedules 1, 2 or 3 of the Public Service Act, 1994 (Act 103 of 1994); or

(ii) any public entity listed in Part A or C of Schedule 3 to the Public Finance Management Act, 1999 (Act 1 of 1999); or

(iii) any other public entity designated by the Minister for the purposes of this Act to be a public authority;

[Definition of 'public authority' substituted by s. 148 (1) (f) of Act 60 of 2001 and by s. 92 (1) (k) of Act 32 of 2004.]

'recipient', in relation to any supply of goods or services, means the person to whom the supply is made;

'registration number' ......

[Definition of 'registration number' deleted by s. 43 (b) of Act 16 of 2004.]

'rental agreement' means-

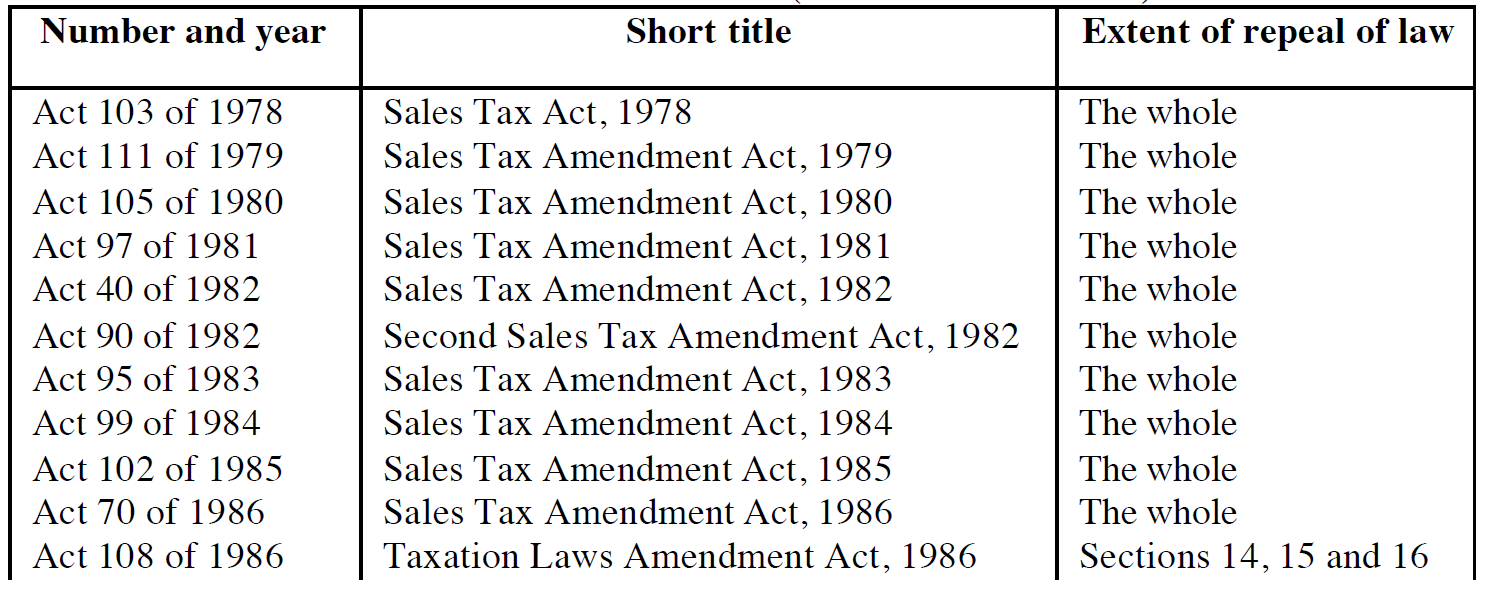

(a) any agreement entered into before, on or after the commencement date for the letting of goods, other than a lease referred to in paragraph (b) of the definition of 'instalment credit agreement' in this section or a financial lease as defined in the Sales Tax Act, 1978 (Act 103 of 1978), prior to its repeal; and

(b) any rental agreement, as defined in the said Act where such agreement is in force on or after the commencement date;

'Republic', in the geographical sense, means the territory of the Republic of South Africa and includes the territorial waters, the contiguous zone and the continental shelf referred to respectively in sections 4, 5 and 8 of the Maritime Zones Act, 1994 (Act 15 of 1994);

[Definition of 'Republic' substituted by s. 18 (b) of Act 37 of 1996.]

'residential rental establishment' ......

[Definition of 'residential rental establishment' substituted by s. 12 (1) (i) of Act 136 of 1992 and deleted by s. 65 (1) (e) of Act 19 of 2001.]

'resident of the Republic' means a resident as defined in section 1 of the Income Tax Act: Provided that any other person or any other company shall be deemed to be a resident of the Republic to the extent that such person or company carries on in the Republic any enterprise or other activity and has a fixed or permanent place in the Republic relating to such enterprise or other activity;

[Definition of 'resident in the Republic' amended by s. 64 (b) of Act 59 of 2000.]

'returnable container' means any container belonging to a class of containers in relation to which, at the time of delivery of the contents thereof, ownership of that container is not transferred to the recipient of the contents and a specifically identified amount is usually charged as a deposit by the supplier of the contents upon the express undertaking of the supplier that upon the return of that container such deposit will be refunded or allowed as a credit to such recipient or any other person returning such container;

'sale' means an agreement of purchase and sale and includes any transaction or act whereby or in consequence of which ownership of goods passes or is to pass from one person to another;

'second-hand goods' means-

(a) goods which were previously owned and used; or

(b) in respect of the transfer of a unit in the circumstances referred to in Item 8 of Schedule 1 to the Share Blocks Control Act, such unit, but does not include-

(i) animals;

[Sub-para. (i) amended by s. 164 (1) (l) of Act 45 of 2003.]

(ii) gold coins contemplated in section 11 (1) (k); and

[Sub-para. (ii) amended by s. 164 (1) (l) of Act 45 of 2003.]

(iii) any prospecting right, mining right, exploration right, production right, mining permit, retention

permit or reconnaissance permit as defined in section 1 of the Mineral and Petroleum Resources

Development Act, 2002 (Act 28 of 2002), or any reconnaissance permission contemplated in section 14 of that Act granted or renewed in terms of that Act or received upon conversion pursuant to Schedule II, except when that prospecting right, mining right, exploration right, production right or interest in that right is transferred, ceded, let, sublet, alienated, varied or otherwise disposed of as contemplated in section 11 of the Mineral and Petroleum Resources Development Act, 2002;

[Sub-para. (iii) added by s. 164 (1) (m) of Act 45 of 2003 and substituted by s. 43 (d) of Act 16 of 2004.]

[Definition of 'second-hand goods' substituted by Government Notice 2695 of 8 November 1991, by s. 12 (1) (j) of Act 136 of 1992 and by s. 9 (1) (j) of Act 20 of 1994.]

'service enterprise' has the meaning assigned thereto in terms of section 21A of the Customs and Excise Act;

[Definition of 'service enterprise' inserted by s. 164 (1) (n) of Act 45 of 2003.]

'services' means anything done or to be done, including the granting, assignment, cession or surrender of any right or the making available of any facility or advantage, but excluding a supply of goods, money or any stamp, form or card contemplated in paragraph (c) of the definition of 'goods';

[Definition of 'services' substituted by Government Notice 2695 of 8 November 1991 and by s. 12 (1) (k) of Act 136 of 1992.]

'share block company' means a share block company as defined in section 1 of the Share Blocks Control Act;

[Definition of 'share block company' inserted by s. 12 (1) (l) of Act 136 of 1992 and substituted by s. 9 (1) (k) of Act 20 of 1994.]

'Share Blocks Control Act' means the Share Blocks Control Act, 1980 (Act 59 of 1980);

[Definition of 'Share Blocks Control Act' inserted by s. 9 (1) (l) of Act 20 of 1994.]

'South African Revenue Service' means the South African Revenue Service established by section 2 of the South African Revenue Service Act, 1997;

[Definition of 'South African Revenue Service' inserted by s. 34 (1) of Act 34 of 1997.]

'specified country' ......

[Definition of 'specified country' deleted by s. 9 (1) (m) of Act 20 of 1994.]

'Stamp Duties Act' means the Stamp Duties Act, 1968 (Act 77 of 1968);

[Definition of 'Stamp Duties Act' inserted by s. 9 (1) (n) of Act 20 of 1994.]

'supplier', in relation to any supply of goods or services, means the person supplying the goods or services;

'supply' includes performance in terms of a sale, rental agreement, instalment credit agreement and all other forms of supply, whether voluntary, compulsory or by operation of law, irrespective of where the supply is effected, and any derivative of 'supply' shall be construed accordingly;

[Definition of 'supply' substituted by s. 81 (1) (f) of Act 53 of 1999.]

'tax' means the tax chargeable under this Act;

[Definition of 'tax' substituted by Government Notice 2695 of 8 November 1991 and by s. 12 (1) (m) of Act 136 of 1992.]

'taxable supply' means any supply of goods or services which is chargeable with tax under the provisions of section 7 (1) (a), including tax chargeable at the rate of zero per cent under section 11;

'tax fraction' means the fraction calculated in accordance with the formula:

___r____

100 + r

in which formula 'r' is the rate of tax applicable under section 7 (1);

'tax invoice' means a document provided as required by section 20;

'tax period', in relation to a vendor, means a tax period determined under section 27;

'this Act' includes the regulations;

'Transfer Duty Act' means the Transfer Duty Act, 1949 (Act 40 of 1949);

[Definition of 'Transfer Duty Act' inserted by s. 9 (1) (o) of Act 20 of 1994.]

'transfer payment' ......

[Definition of 'transfer payment' inserted by Government Notice 2695 of 8 November 1991 and by s. 12 (1) (n) of Act 136 of 1992, substituted by s. 23 (1) (g) of Act 27 of 1997 and by s. 148 (1) (g) of Act 60 of 2001 and deleted by s. 164 (1) (o) of Act 45 of 2003.]

'transitional metropolitan council' means a transitional metropolitan council as defined in section 1 of the Local Government Transition Act, 1993 (Act 209 of 1993);

[Definition of 'transitional metropolitan council' inserted by s. 9 (1) (p) of Act 20 of 1994.]

'trust fund' means any fund consisting of cash or other assets the administration and control of which is entrusted to any person acting in a fiduciary capacity by any person, whether under a deed of trust or by agreement, or by a deceased person under a will made by that person;

[Definition of 'trust fund' substituted by s. 21 (d) of Act 136 of 1991.]

'unconditional gift' ......

[Definition of 'unconditional gift' deleted by s. 92 (1) (l) of Act 32 of 2004.]

'VAT registration number', in relation to any vendor, means the number allocated to that vendor by the Commissioner for the purposes of this Act;

[Definition of 'VAT registration number' inserted by s. 43 (e) of Act 16 of 2004.]

'vendor' means any person who is or is required to be registered under this Act: Provided that where the Commissioner has under section 23 or 50A determined the date from which a person is a vendor that person shall be deemed to be a vendor from that date;

[Definition of 'vendor' amended by s. 23 (1) (h) of Act 27 of 1997.]

'welfare organisation' means any public benefit organisation which is exempt from income tax in terms of section 10 (1) (cN) of the Income Tax Act, if it carries on or intends to carry on any welfare activityi* determined by the Minister for purposes of this Act, relating to those activities that fall under the headings-

(a) welfare and humanitarian;

(b) health care;

(c) land and housing;

(d) education and development; or

(e) conservation, environment and animal welfare.

[Definition of 'welfare organization' substituted by s. 21 (e) of Act 136 of 1991, by Government Notice 2695 of 8 November 1991, by s. 12 (1) (o) of Act 136 of 1992, by s. 81 (1) (g) of Act 53 of 1999 and by s. 148 (1) (h) of Act 60 of 2001, amended by s. 114 (1) (c) of Act 74 of 2002 and substituted by s. 92 (1) (m) of Act 32 of 2004.]